"THE TREASURY BOSS AND THE PAWNSHOP OF AOTEAROA: How a White Supremacist Government Hocked the Nation's Taonga to Faceless Loan Sharks — Then Sent the Bill to Whānau" - 19 February 2026

They sold the waka. They don't know who bought it. And now they're charging whānau rent to sit in it.

Mōrena ano Aotearoa,

The Pawnshop Opens for Business

Imagine a pawnshop. Not the kind on a tired suburban strip — the kind that operates in the dark, behind glass so thick you cannot see who sits on the other side.

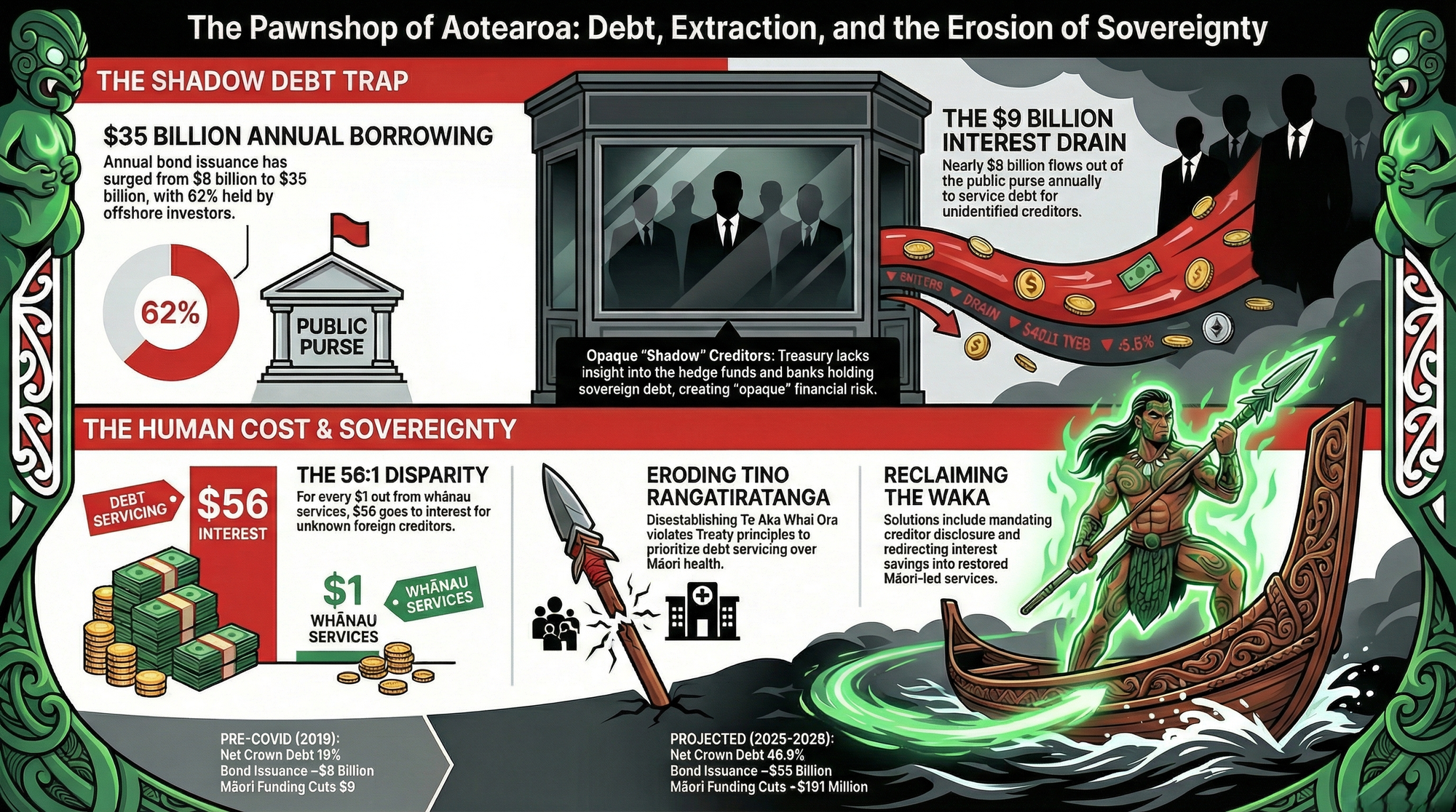

Now imagine the owner of a great waka hourua — a double-hulled voyaging canoe, built over generations, carved with the whakapapa of a people — walks into that pawnshop, hands the waka over the counter, and says: "Give me $35 billion. I don't need to know your name."

That is what the New Zealand Government is doing. Every year. Right now.

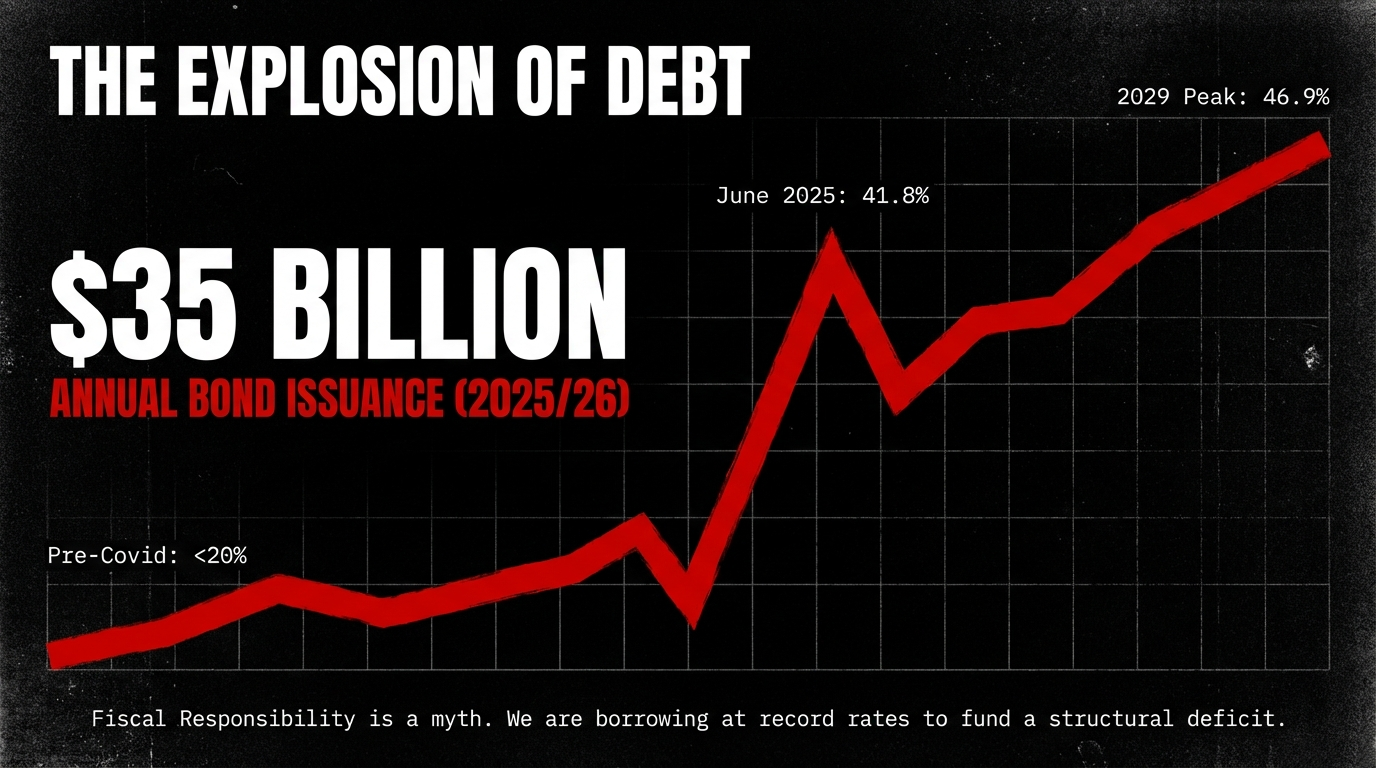

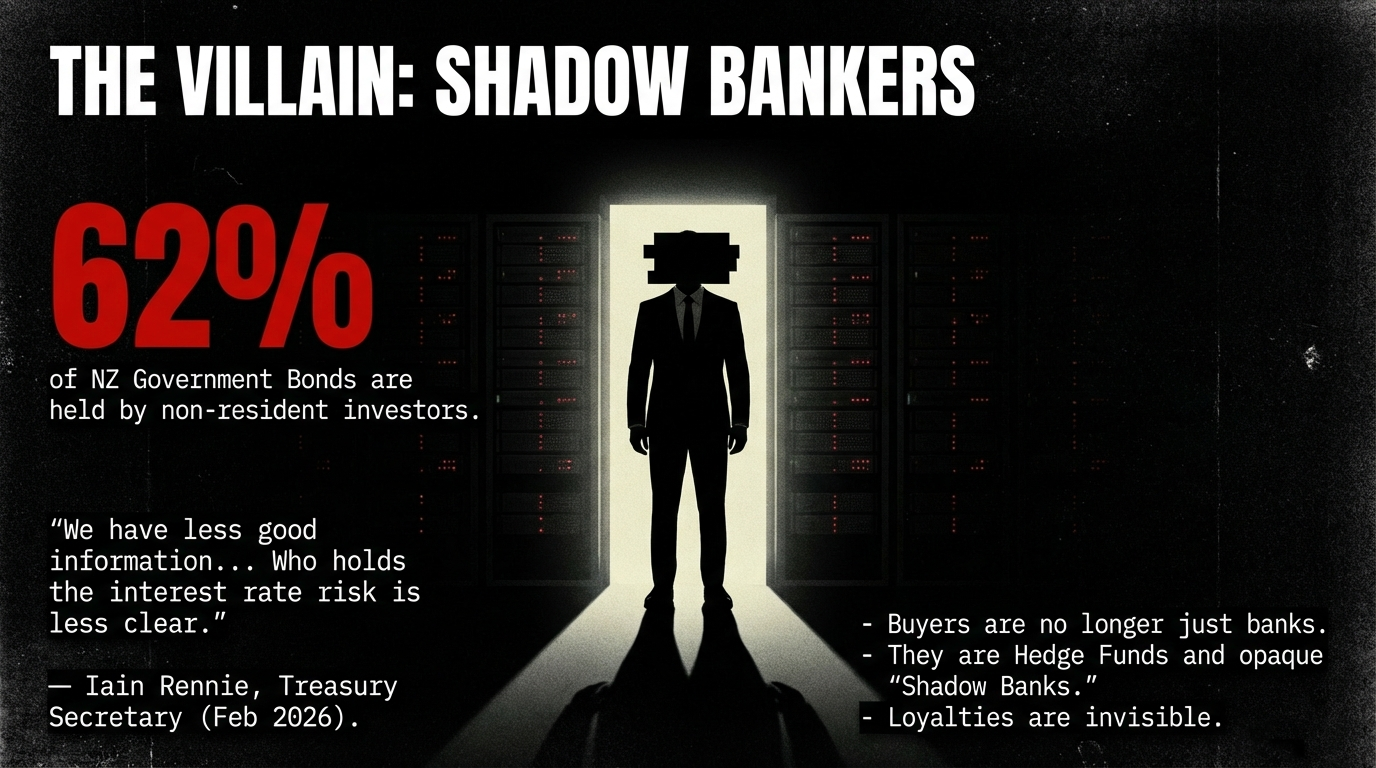

On 17 February 2026, Treasury Secretary Iain Rennie — the most senior fiscal official in Aotearoa — told the NZ Herald that the Government has less insight into who owns its bonds than at any point since the Global Financial Crisis. Before 2020, the Crown issued about $8 billion in Government Bonds a year. The forecast for 2025/26 is $35 billion. Around 60% of those bonds are sold to offshore investors. Hedge funds. Pension funds. Shadow banks. Entities whose structures, leverage, and loyalties are, in Rennie's own word, "opaque."

"Who holds the interest rate risk, who holds the exchange rate risk is less clear. We have less good information," Rennie said.

Translation for the Western mind: the Government is writing cheques to people it cannot identify, at interest rates it cannot control, using money it does not have, to pay for services it is simultaneously cutting.

And the interest on those cheques? Nearly $9 billion a year — pouring out of the public purse and into the vaults of strangers, while kaiāwhina lose their jobs, Whānau Ora loses its funding, and Māori tamariki lose seven years of life expectancy compared to their Pākehā peers.

The Waka Has Been Stripped: The Numbers They Cannot Hide

Let us be precise about the wreckage.

Net core Crown debt reached $182.2 billion — 41.8% of GDP — at 30 June 2025, as confirmed by Treasury's Financial Statements. Before Covid, it was below 20%. According to the Half Year Economic and Fiscal Update 2025, debt is forecast to peak at 46.9% of GDP in 2028-29.

Nicola Willis — the Finance Minister who campaigned on turning the debt track below 40% — now presides over a projected $13.9 billion deficit for 2025/26, as reported by RNZ. A surplus is not forecast until 2029/30. The Budget 2025 Fiscal Strategy Report identifies a structural OBEGALx deficit averaging 1.1% of GDP — meaning the books are bleeding even after you strip out the recession.

The NZ Debt Management Office confirms gross NZGB issuance of $175 billion over the forecast period through June 2029. As at May 2025, 62% of NZGBs were held by non-resident investors, per the NZDMO Securities Overview.

The Government is renewing its Covid-era debt at higher interest rates. It is issuing more debt to cover the interest bill. And it is issuing even more debt to pay for new spending — all while Nicola Willis stands at the podium and calls it "fiscal responsibility."

This is not a government managing debt. This is a government addicted to it — and the dealers are invisible.

The Shadow Bankers: Who Owns the Pawnshop?

Here is the part that should make every New Zealander's blood run cold.

The people buying our bonds are not the regulated, transparent banks of the pre-GFC era. They are non-bank financial institutions (NBFIs) — the shadow banking sector — and their rise has been documented with alarm by the most senior financial authorities on the planet.

Pablo Hernández de Cos, General Manager of the Bank for International Settlements, delivered a lecture at the London School of Economics on 27 November 2025 titled "Fiscal threats in a changing global financial system". Rennie explicitly cited this speech at the 2026 NZ Economics Forum. The BIS findings are devastating:

- NBFIs now hold approximately half of the world's financial assets.

- Hedge funds use the "cash-futures basis trade" — a leveraged bet on the gap between bond prices and futures — financed through repo markets at zero haircuts on approximately 70% of US dollar bilateral repos.

- The FX swap market — the mechanism cross-border bondholders use to hedge currency risk — has reached $130 trillion outstanding, with three quarters of contracts maturing in less than one year.

- This creates a "bank-NBFI-sovereign nexus" where stress in repo markets can trigger FX swap rollovers, which can trigger a global dollar scramble, which can spike the borrowing costs of every small open economy on earth.

The IMF's October 2025 Global Financial Stability Report confirmed that banks in the US and eurozone now have NBFI exposures that exceed their Tier 1 capital — the buffer meant to absorb losses. The IMF warned that NBFIs "amplify shocks through private credit, real estate, and crypto".

Rennie stated it plainly in his full speech: "We don't always know who owns our sovereign debt, and the behaviour of these players in an interconnected financial system can be opaque."

The metaphor completes itself: the waka has been pawned to loan sharks who operate behind one-way glass, who can call in the debt at any moment, and whose leverage is so extreme that when one stumbles, the entire global credit system lurches.

And Aotearoa — borrowing $35 billion a year with 62% going offshore through exactly these channels — is chained to the hull.

Three Examples for the Western Mind: The Harm Made Visible

For those raised in the Western tradition, the concept of mauri — the life force that animates all living things, places, and communities — may seem abstract. It is not. Mauri is as measurable as a bond yield, as real as a deficit, as consequential as a child's life expectancy. The destruction of mauri is what happens when a government prioritises payments to invisible creditors over the breath of its own people.

Here are three examples that translate the tikanga violation into terms the Western mind can grasp.

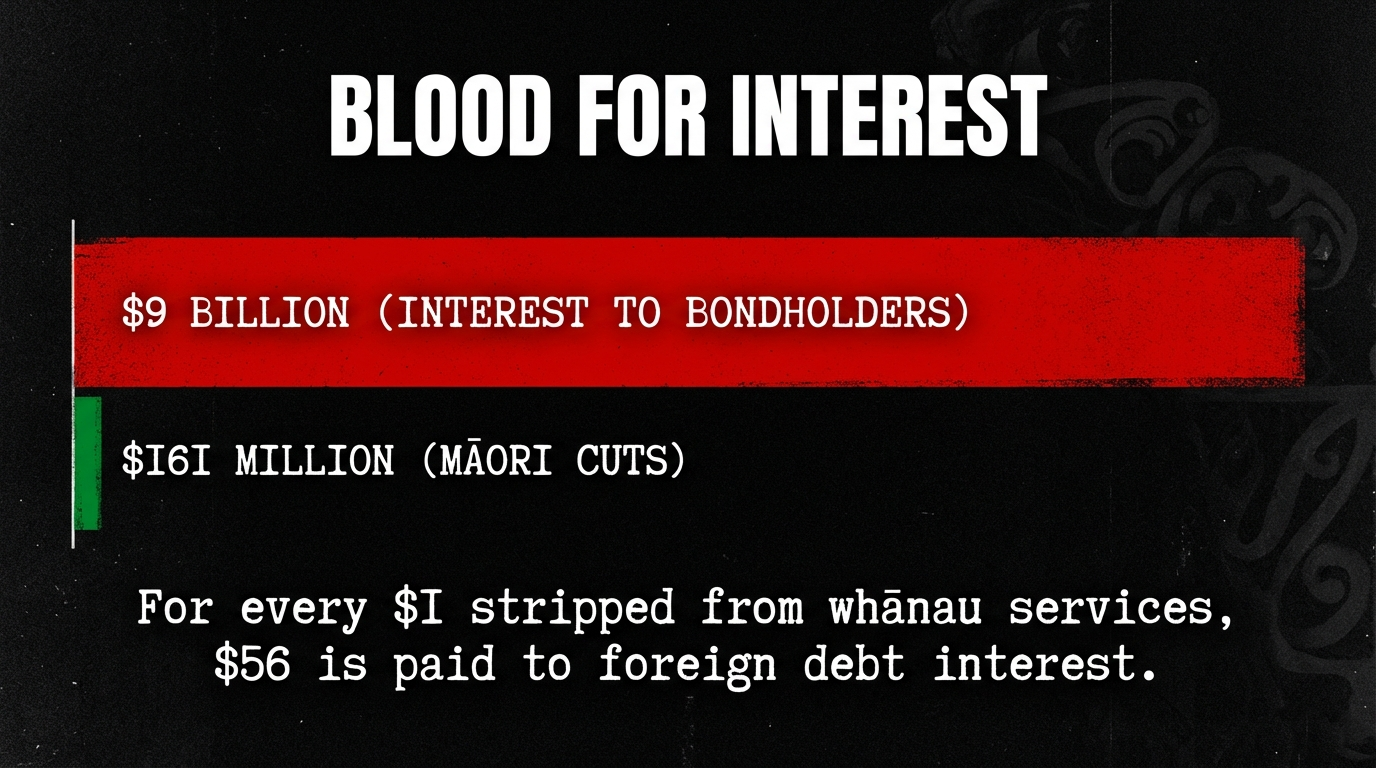

Example 1: The $9 Billion vs. $161 Million — Or, Paying the Loan Shark While Starving the Children

The harm: In the year to June 2025, the Crown's interest bill hit nearly $9 billion, flowing to bondholders — many of whose identities the Government cannot identify. Meanwhile, Māori-specific funding cuts across Budget 2024 and 2025 total approximately $161 million: $25 million from Whānau Ora, $35.5 million from the Māori Health Authority at its disestablishment, $8.5 million from kaiāwhina roles, $33 million from Māori housing, $54 million from Whai Kāinga Whai Oranga, and $5 million from the Māori Development Fund.

The ratio: For every dollar stripped from whānau, approximately $56 goes to servicing debt held by unknown foreign creditors.

The Western parallel: Imagine a family earning $80,000 a year. They owe money to a payday lender whose name they don't know. They spend $9,000 a year on interest payments to that lender. Simultaneously, they cancel their children's health insurance ($161), claiming they can't afford it. That is what this government is doing — at a national scale, with your children's lives.

The tikanga violation: In te ao Māori, manaakitanga — the obligation to care for and uplift others — is not optional. It is the foundational ethic of governance. A rangatira who feeds strangers while their own whānau starve is not exercising mana — they are committing a form of spiritual theft. The $9 billion interest bill flowing to opaque offshore entities while whānau services are gutted represents a direct destruction of manaakitanga at the Crown level. The mauri of the community is depleted not by accident, but by policy design.

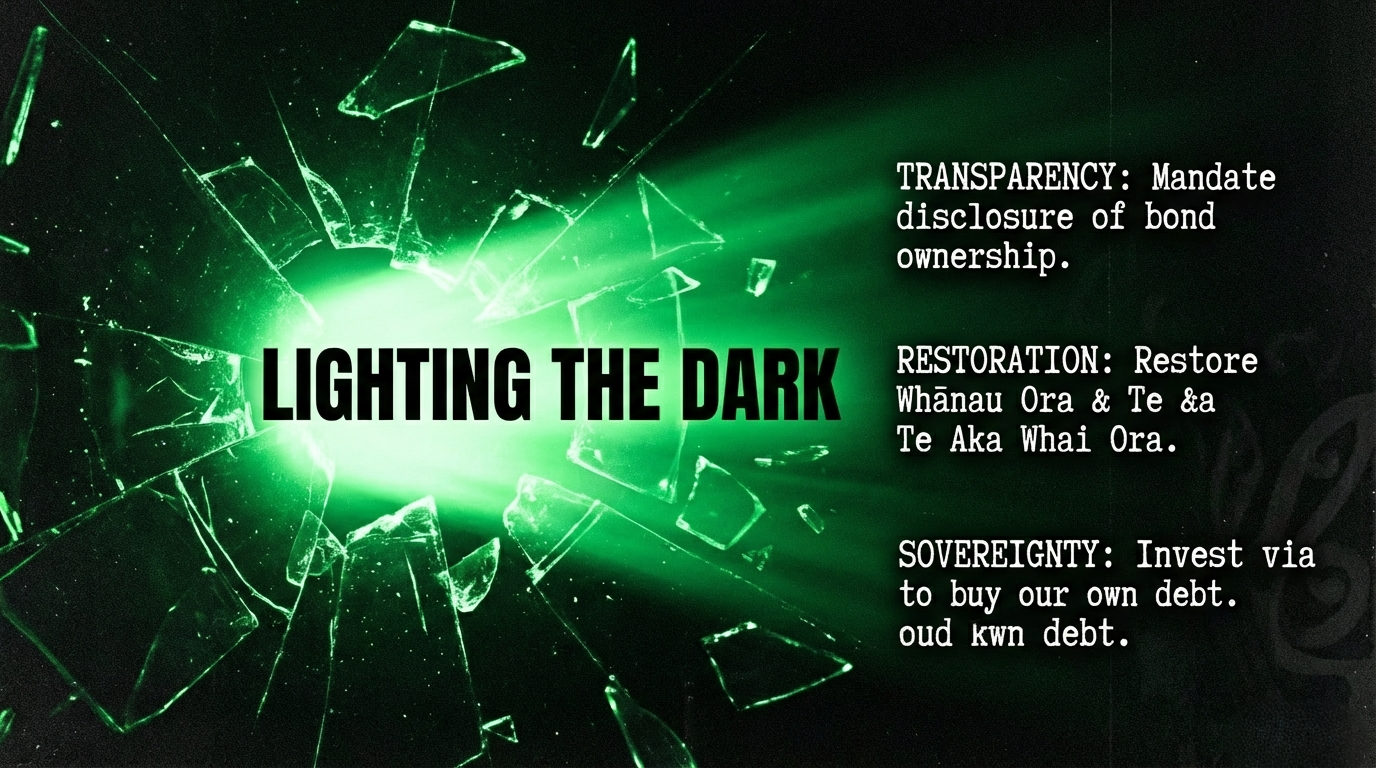

The solution: Mandate disclosure of ultimate beneficial ownership of NZ Government Bonds above threshold holdings. If the Overseas Investment Office can demand to know who buys a dairy farm, the Crown can demand to know who holds its sovereign debt. Redirect a fraction of the $9 billion interest bill into restored Whānau Ora and kaiāwhina services — even 1% ($90 million) would exceed every Māori-specific cut combined.

As covered previously by The Māori Green Lantern in "The Mirage of Prosperity: Exposing the Colonial and Neoliberal Myths of Corporate Tax Cuts" and "Aotearoa's Health System: A Neoliberal Nightmare of Mismanagement and Broken Promises", this government's fiscal framework is structurally designed to extract wealth from the vulnerable and channel it to the privileged — whether through unfunded tax cuts or interest payments to invisible creditors.

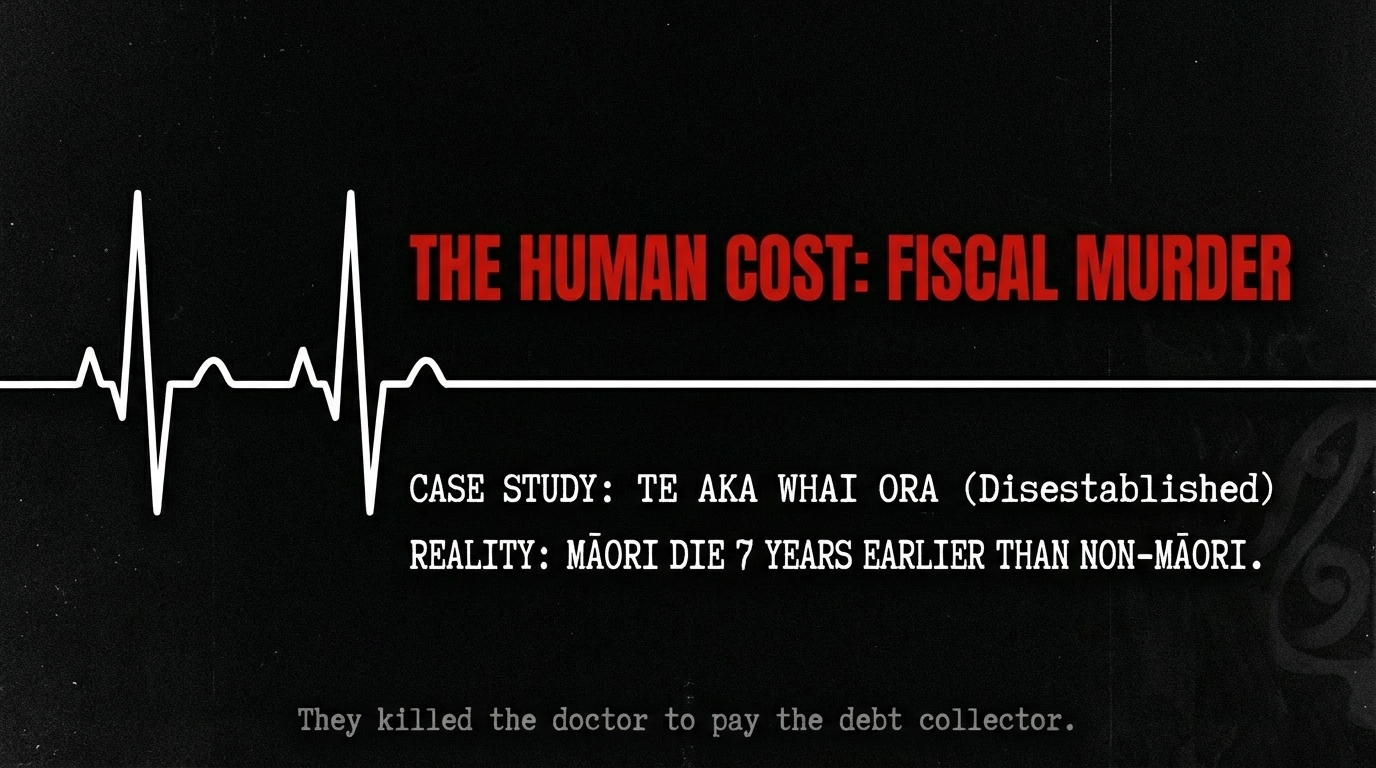

Example 2: Te Aka Whai Ora — Killing the Doctor to Pay the Debt Collector

The harm: Te Aka Whai Ora, the Māori Health Authority, was disestablished under urgency in March 2024, just two years into its existence. 740 doctors signed a letter opposing the move. The Waitangi Tribunal found the Crown breached Treaty principles of tino rangatiratanga, good government, partnership, active protection, and redress. In May 2025, the Tribunal was told directly that the mainstream health system was failing Māori.

Māori die seven years earlier than non-Māori. The life expectancy gap has barely shifted in decades.

The Western parallel: Imagine a hospital in a low-income neighbourhood — the only one that speaks the patients' language, understands their culture, and has finally started reducing their mortality rates. The Government shuts it down under urgency, without consultation, to save $35.5 million. The same Government then spends $9 billion that year on interest payments to creditors it cannot name. That is not fiscal discipline. That is fiscal murder.

The tikanga violation: Tino rangatiratanga — the right of Māori to exercise authority over their own health, their own bodies, their own systems of care — was guaranteed under Article Two of Te Tiriti o Waitangi. Te Aka Whai Ora was the first structural expression of that right in the health system. Its destruction was not merely a budgetary decision. It was a violation of whakapapa — severing the institutional lineage that connected whānau to culturally grounded healthcare. In te ao Māori, to destroy the structure that protects the people's hauora (health and wellbeing) is to attack the mauri of the iwi itself.

The solution: Restore Te Aka Whai Ora with statutory protection against future disestablishment without Waitangi Tribunal consent. Fund it from the structural savings that transparency in bond markets would generate. The Tribunal has already found the Crown in breach — the legal and moral mandate is already written.

As previously analysed by The Māori Green Lantern in "The Three-Headed Dragon of Colonial Power: How New Zealand's Coalition Government Masks White Supremacy Behind 'Unity' Rhetoric", the disestablishment of Te Aka Whai Ora was never about money. It was about dismantling the institutional infrastructure of Māori self-determination — brick by brick, vote by vote, urgency motion by urgency motion.

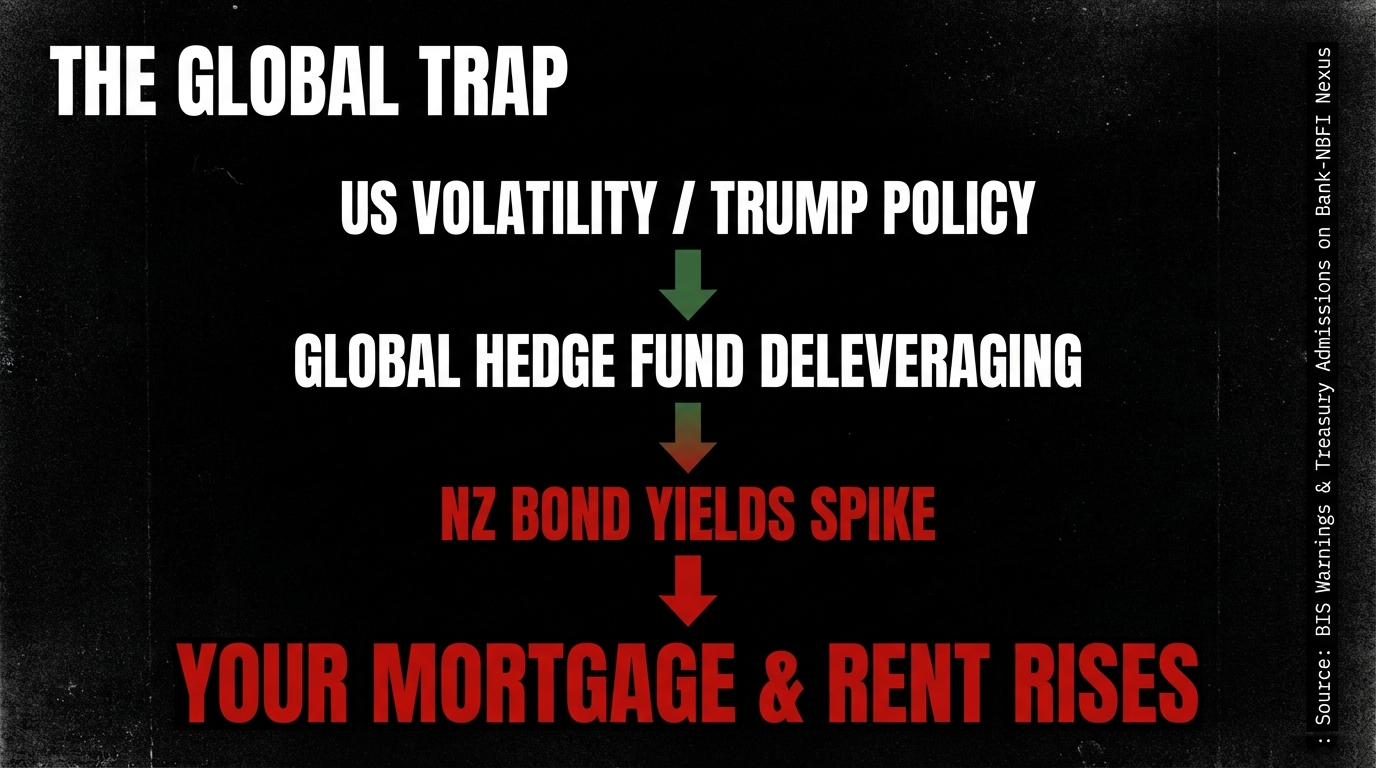

Example 3: The Trump Transmission Channel — Or, How a Fascist in Washington Spikes Your Mortgage in Manurewa

The harm: Rennie explicitly warned that President Donald Trump's pressure on the Federal Reserve to lower US interest rates could paradoxically raise New Zealand's borrowing costs. If US investors demand higher returns on Treasuries due to fears about American fiscal sustainability or inflation, they demand even higher returns on NZ bonds. Rennie cited Reserve Bank research showing NZ bond rates are closely correlated to the US market. The BIS confirmed that the April 2025 US Treasury market volatility was driven partly by hedge fund deleveraging — exactly the opaque actors now holding 62% of our debt.

The quantified risk: The EU ESRB's 2025 Non-bank Financial Intermediation Risk Monitor found hedge funds have increased their leverage in sovereign bond markets, particularly in basis trades. When these trades unwind — as they did violently in March 2020 — yields spike, borrowing costs surge, and small open economies get crushed. New Zealand, issuing $35 billion a year through these exact channels, is strapped to the mast of a ship steered by a man who thinks tariffs are monetary policy.

The Western parallel: You are a homeowner in Manurewa. Your mortgage rate is influenced by wholesale interest rates, which are influenced by government bond yields, which are influenced by global sovereign debt markets, which are influenced by hedge funds unwinding leveraged bets on US Treasuries, which are influenced by Donald Trump posting threats at the Federal Reserve on Truth Social at 3am. That is the chain. That is the transmission channel. And this government has no plan to insulate you from it — because it is too busy relaxing foreign investment rules and courting the same global capital that holds the whip.

The tikanga violation: The concept of whanaungatanga — the interconnection of all things, the web of relationships that sustains the collective — extends beyond human relationships to encompass economic sovereignty. When a government surrenders fiscal autonomy to opaque global markets, it severs the whanaungatanga between the state and its people. Decisions about whānau wellbeing are made not in the Beehive but in the trading rooms of hedge funds in Connecticut and London. The mauri of economic self-determination — what our tūpuna fought for at Ōrākau, at Gate Pā, at Parihaka — is traded away for a basis point on a bond yield.

The solution: Expand KiwiSaver and NZ Super Fund allocations to NZGBs to reduce offshore dependence — not halve KiwiSaver employer contributions as Budget 2025 did. Advocate internationally for the minimum haircut and central clearing reforms the BIS recommends. Implement a sovereign wealth fund model that prioritises domestic bond absorption over foreign dependence.

As covered by The Māori Green Lantern in "Selling Paradise: How Neoliberalism and Foreign Billionaires Exploit Aotearoa's Whenua" and "Bloodless Conquest: How Capitalist Nomads Carve Aotearoa While Tangata Whenua Bear the Scars", the pattern is always the same: open the door to foreign capital, remove the safeguards, cut the services, and call it growth. The only thing growing is the debt — and the distance between the Crown and its obligations to tangata whenua.

Five Hidden Connections: The Architecture of Extraction

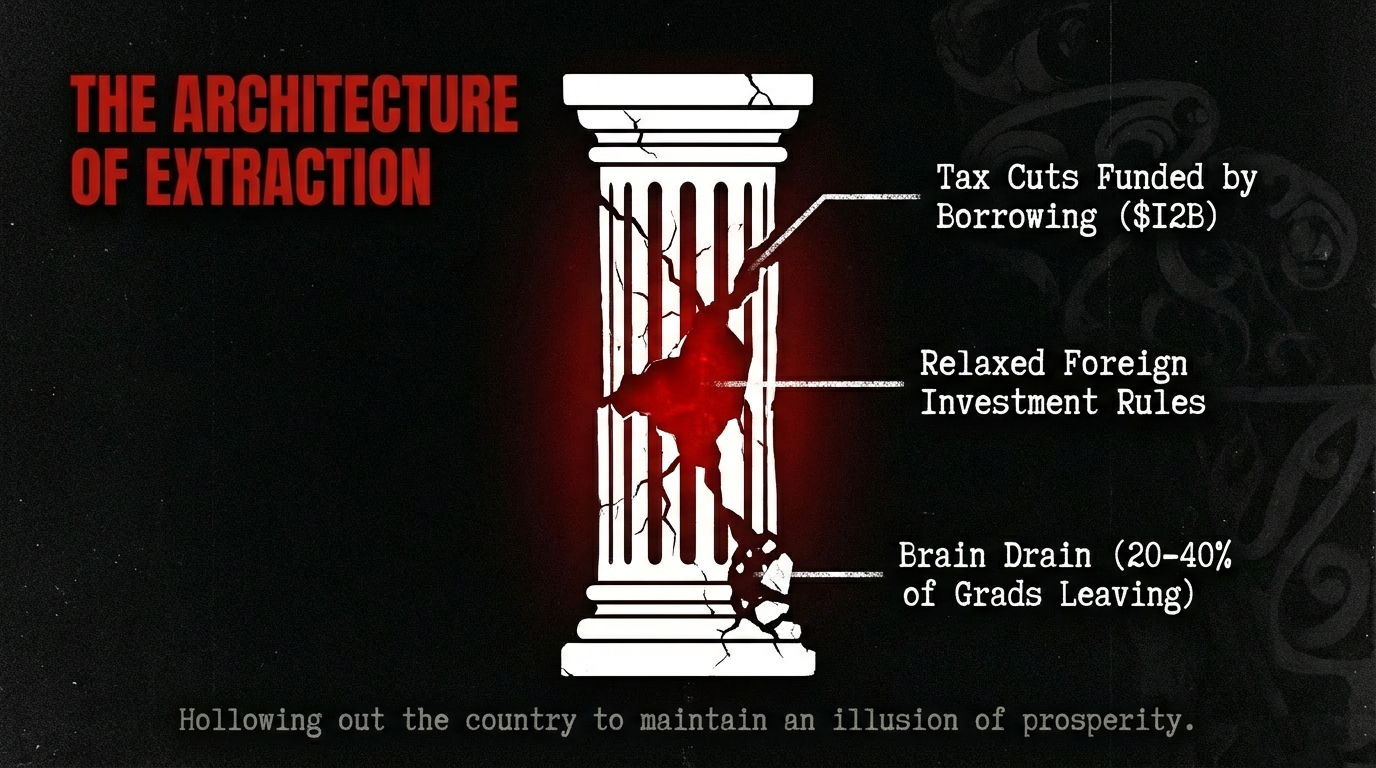

Connection 1: Tax Cuts Financed by Faceless Foreign Debt

Willis delivered tax cuts that RNZ reported were costed at approximately $12 billion in borrowing. NZ borrowing has increased 11% year-on-year, total debt reaching $238.8 billion. The structural deficit requiring this ongoing borrowing is partly a product of those tax cuts — money borrowed from opaque foreign creditors to give tax relief disproportionately benefiting higher earners.

Willis's defence? "This is why you should be scrutinising those who say they will spend more." But the HYEFU showed the deficit was $1.8 billion worse than the May forecast. The woman who promised to turn the debt track around is driving it off a cliff — and handing the steering wheel to hedge funds whose names she does not know.

Connection 2: Relaxing Foreign Investment Rules While Losing Track of Foreign Creditors

The same Government that cannot tell you who holds 60% of its debt is simultaneously relaxing foreign investment rules through the Overseas Investment Amendment Bill. The Bill shifts the regime from requiring investors to demonstrate benefit to New Zealand, to a starting presumption that investment should proceed unless national interest risks are identified.

Luxon announced Invest New Zealand to court foreign capital. Meanwhile, he floated selling state assets if re-elected. Borrow from strangers. Sell to strangers. Cut the whānau. Call it vision.

Connection 3: The Credit Rating Trap as Colonial Discipline

S&P (AA+ stable), Fitch (AA+ stable), and Moody's (Aaa stable) function as the overseers of the neoliberal plantation. S&P warned the rating could be lowered if the deficit does not narrow. Willis weaponises these ratings against domestic opponents, declaring that alternative spending proposals would send "our credit rating plummeting."

But the ratings framework incentivises cutting public services to maintain favourable borrowing terms for the very opaque creditors whose behaviour in a crisis is unpredictable. S&P's own analyst Martin Foo stated that New Zealand's standard of living was "going backwards." The prescription — austerity for the people, red carpets for capital — is the disease masquerading as the cure.

Connection 4: The Brain Drain as Fiscal Confession

Rennie's speech revealed a data point the Government would rather bury: 20-40% of New Zealand graduates leave the country. NZ capital intensity is roughly 50% of OECD comparators. The Government is not merely failing to invest in infrastructure and services — it is producing a country so hollowed out that its best-educated young people flee to Australia, taking their tax contributions with them and leaving behind a shrinking base to service an expanding debt.

Treasury's own Long-term Fiscal Statement projects that without policy changes, debt could rise to approximately 200% of GDP by 2065, as reported by RNZ. The pawnshop analogy breaks down at this point — because even a pawnshop requires collateral. What collateral does a nation have when its young have left and its services have been gutted?

Connection 5: The Fiscal Cost of Shocks — And Who Pays

Rennie's speech contained a devastating admission: "Since the late 1980s, the fiscal cost of government responses to economic shocks has averaged around 10% of GDP every decade. But the cost of these responses has not been matched by savings between shocks."

Read that again. Every decade, we spend 10% of GDP responding to crises. And we never save enough between crises to cover the next one. The result is a ratchet — each crisis adds debt, each recovery fails to clear it, and the interest payments compound. The whānau who bear the cost of both the crisis (through job losses, service cuts) and the recovery (through austerity, benefit freezes) are the same whānau every time. Māori. Working class. Regional. Disabled. The opaque creditors who collect the interest? They bear no cost at all. They are faceless, borderless, and consequence-free.

The Mauri Deficit: A Ledger of Destruction

| Metric | Pre-Covid (2019) | Current (2025) | Projected Peak |

|---|---|---|---|

| Net core Crown debt (% GDP) | 19% | 41.8% | 46.9% (2028) |

| Annual bond issuance | ~$8b | $35b | Sustained $30b+ |

| Crown interest bill | ~$3b | ~$9b | Rising |

| Offshore bond ownership | ~55% | 62% | Trending up |

| Structural deficit | Surplus | -1.1% GDP avg | Surplus not until 2029/30 |

| Māori-specific funding cuts | — | ~$161m across 2 Budgets | Ongoing |

| Māori life expectancy gap | 7 years | 7 years | Unchanged |

Sources: NZ Treasury, Budget 2025 FSR, NZDMO, ASMS, Waatea News

The Pawnshop Must Be Shut Down

The taiaha of truth cuts through the fog. Treasury Secretary Iain Rennie — hardly a revolutionary — is telling us the Government does not know who holds its own debt. He is telling us global conditions outside our control can spike borrowing costs overnight. He is telling us the structural deficit demands hard choices.

Those choices have already been made. They were made when Te Aka Whai Ora was murdered under urgency. When kaiāwhina lost their jobs. When Whānau Ora lost its funding. When the Māori Development Fund was bled dry. When $12 billion in tax cuts were borrowed from opaque foreign creditors so National voters could save a few dollars a week while Māori tamariki continue to die seven years before their time.

$9 billion a year leaves the people of Aotearoa and flows to bondholders — many of whose identities the Government itself cannot identify. The total Māori-specific cuts across two Budgets amount to roughly $161 million. For every dollar stripped from whānau, $56 goes to servicing debt held by strangers.

This Government did not inherit a pawnshop. It built one. It stocked the shelves with our taonga. It installed one-way glass so the creditors remain invisible. And it hired Nicola Willis to stand at the counter and tell whānau they need to tighten their belts.

We call it what it is: fiscal colonisation dressed in a spreadsheet.

The waka was built by our tūpuna. The debt was created by this Government. The creditors are faceless. And the whānau — as always — are paying.

Ko te pae tāwhiti whāia kia tata. Ko te pae tata whakamaua kia tina.

Seek the distant horizon and bring it near. Grasp the horizon that is close and make it secure.

The horizon is clear. The pawnshop must be shut down. The waka must be reclaimed.

Kia mau ki te waka. Kia kaha. Kia manawanui.

Hold fast to the waka. Be strong. Be resolute.

Koha Consideration

Every koha signals that whānau are ready to fund the accountability that neither the Crown, nor the opaque hedge funds collecting $9 billion a year in interest, nor the credit rating agencies enforcing austerity will ever provide.

It signals that rangatiratanga includes the power to fund our own truth-tellers — because when Treasury admits it doesn't know who holds our debt, and the Government keeps borrowing anyway, someone must stand in the gap and demand answers on behalf of the people who pay the price.

Kia kaha, whānau. Stay vigilant. Stay connected. And if you are able, consider a koha to ensure the light keeps shining on the pawnshop they built on our whenua.

If you are unable to koha, no worries! Subscribe or follow The Māori Green Lantern, kōrero and share with your whānau and friends — that is koha in itself. Every share is a brick pulled from the one-way glass.

Three pathways exist:

Koha — Support: https://app.koha.kiwi/events/the-maori-green-lantern-fighting-misinformation-and-disinformation-ivor-jones

Subscribe to the Māori Green Lantern: https://www.themaorigreenlantern.maori.nz/#/portal/support

Direct bank transfer: HTDM, account number 03-1546-0415173-000.

Ivor Jones The Māori Green Lantern Fighting Misinformation And Disinformation From The Far Right

Research conducted 19 February 2026. Sources consulted: NZ Treasury, NZDMO, NZ Herald, RNZ, 1News, Bank for International Settlements, IMF Global Financial Stability Report, EU ESRB, Waitangi Tribunal, NZ Budget documents, ASMS, Waatea News, S&P Global Ratings, Fitch Ratings, The Spinoff, Chambers & Partners. All URLs verified at time of research.