"THE KIWISAVER CONJURER'S TRICK" - 22 June 2026

How National's Compulsory Savings Pitch Abandons the People It Claims to Serve

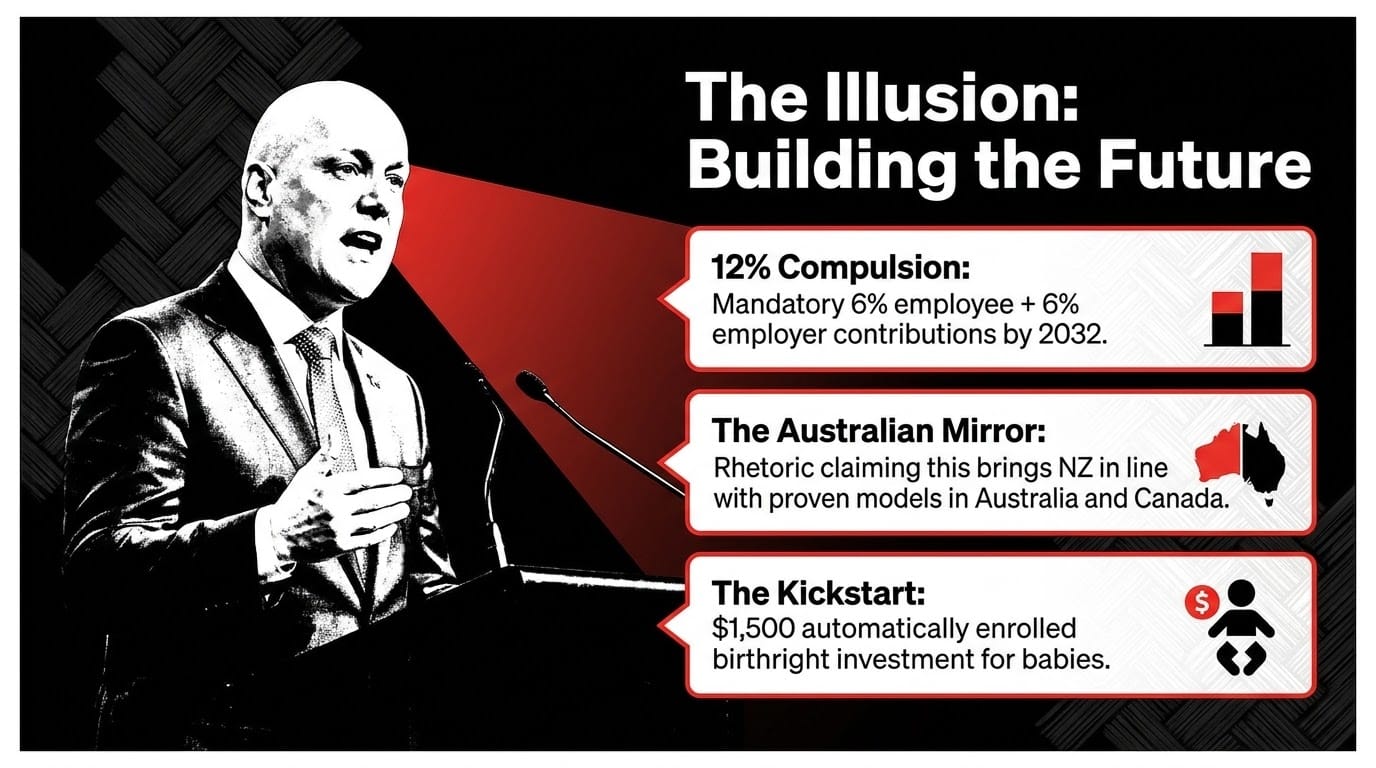

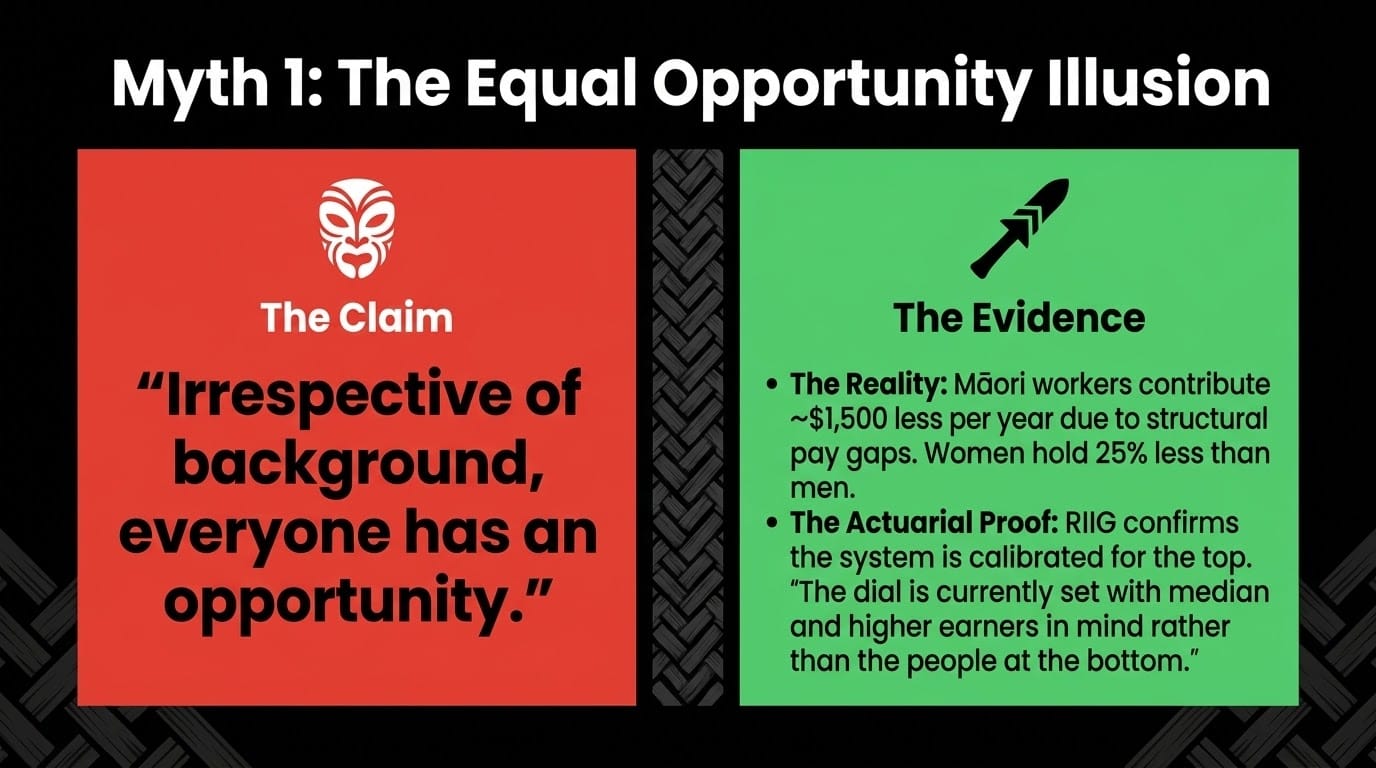

"There are things that we can do to improve the programme and make it even stronger, so that actually, irrespective of your background or your circumstances, everyone's got an opportunity to build wealth over time."

— Christopher Luxon, Morning Report, 22 June 2026

He kōrero tāhae. A stolen speech.

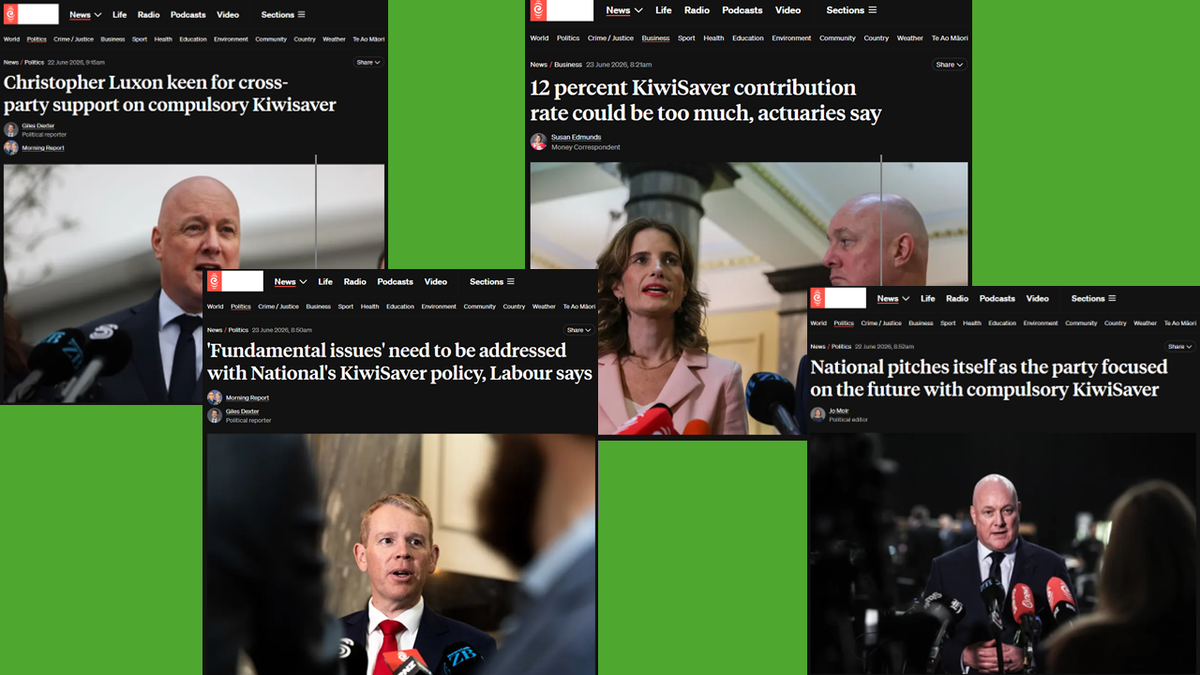

The man who helped gut KiwiSaver now wants a standing ovation for rebuilding it — and the New Zealand media, true to form, handed him one. Two RNZ pieces published on 22 June — one a straight news report by Giles Dexter, the other a strategy analysis by Jo Moir — described National's compulsory KiwiSaver announcement at the party's 90th Annual General Meeting as a bold vision for the future.

Between them, they repeated National's claims almost without challenge: that the policy will help everyone "irrespective of background or circumstances," that Australia proves the model works, that the Budget can fund it, and that cross-party consensus should be a given.

Within 24 hours, two more sources delivered their verdict — from opposite ends of the political and professional spectrum. The NZ Society of Actuaries' Retirement Income Interest Group (RIIG) published findings that 12% combined KiwiSaver contributions — the exact rate National proposes by 2032 — could be

"excessive" for minimum wage earners and "over-egging it" for median earners.

Labour publicly named "fundamental issues" that must be resolved before any cross-party consensus is possible.

Every one of National's claims is demonstrably false. The evidence is publicly available, peer-reviewed, government-sourced — and now confirmed by actuaries and the parliamentary opposition.

This essay names the lies, traces the pattern, and documents the harm.

E tū ana tātou — we stand together.

🎙️ The Deep Dive Podcast

Listen to a lively conversation between two hosts, unpacking and connecting every thread of this investigation — including the actuaries' findings, Labour's response, and the super age trap. The Deep Dive Podcast is embedded on the essay page at www.themaorigreenlantern.maori.nz.

I apologise in advance for the AI's very harsh pronunciation of te reo Māori. Please don't shoot me. 😊

📺 YouTube

Short video supporting the essay — same apology applies for the AI's pronunciation of reo! 😊

The Record: National Stole From KiwiSaver Four Times Before Proposing to Save It

Let's begin with the most brazen conjurer's trick in recent New Zealand political history.

Luxon, when confronted on Morning Report about National's history of KiwiSaver cuts, dismissed it:

"this was now a different party."

Jo Moir's analysis piece gently noted that "a previous iteration of a National government once scrapped the country's then-compulsory retirement savings scheme," then moved on.

Neither interrogated the specific, quantified damage National has done.

Here is what National actually did — verified from primary government sources:

Cut 1 — 2011: National's Budget 2011 ended the tax-free status of employer contributions, subjecting them to Employer Superannuation Contribution Tax (ESCT) at each employee's marginal tax rate — meaning the actual value of the employer contribution landing in members' accounts was silently reduced. In the same Budget, National halved the annual Member Tax Credit from a maximum of $1,042 to $521, stripping over $500 million per year from KiwiSaver members.

Cut 2 — 2012: The Retirement Commission's own history of KiwiSaver confirms: minimum contribution rates were cut from 4% to 2% for members, and employer compulsory contributions were capped and reduced.

Cut 3 — 2015: On 20 May 2015, Finance Minister Bill English abolished the $1,000 KiwiSaver Kick-Start payment from 2pm that afternoon, with no notice to prospective members. The Beehive's own press release states this would "save over $500 million over the next four years." The Green Party documented the full record: "It was National that removed the $1,000 kick-start... It was National that introduced a new tax on employer contributions to KiwiSaver in 2011. It was National that halved the annual maximum Government contribution."

Cut 4 — 2025: In the same Budget under which they are now announcing compulsory KiwiSaver, National halved the government contribution again. From 1 July 2025, the maximum annual government top-up was reduced from $521.43 to $260.72 — 25 cents for every dollar contributed, down from 50 cents.

The same government that has cut KiwiSaver's government contribution four times since 2011 — ripping billions out of ordinary New Zealanders' retirement accounts — is asking you to applaud its commitment to your future.

Confidence level: Verified. Every figure confirmed by Beehive, IRD, and Retirement Commission sources.

Claim: "Irrespective of Your Background or Circumstances, Everyone's Got an Opportunity"

This is the most dangerous lie in Luxon's entire pitch, repeated almost verbatim in both RNZ pieces.

The evidence shows the opposite: KiwiSaver is a system that systematically rewards wealth and punishes poverty — and compulsion will lock those inequities in permanently.

The Māori Gap

Te Ara Ahunga Ora, the Retirement Commission, has documented this clearly: "Māori receive NZ Superannuation for fewer years, have lower KiwiSaver balances because they tend to earn less, and are less likely to own their own home in retirement." AUT infographic data shows Māori and Pacific workers contributing under $2,000 annually to KiwiSaver, compared to $2,821 for European workers. The Retirement Commission's own research confirms: if you are Māori or Pacific, you are likely to have around $1,500 less contributed into your KiwiSaver account annually than a European person — not because of different rates, but because of the structural pay gap embedded in New Zealand's economy.

The Actuaries Confirm: The System Is Set for the Middle, Not the Bottom

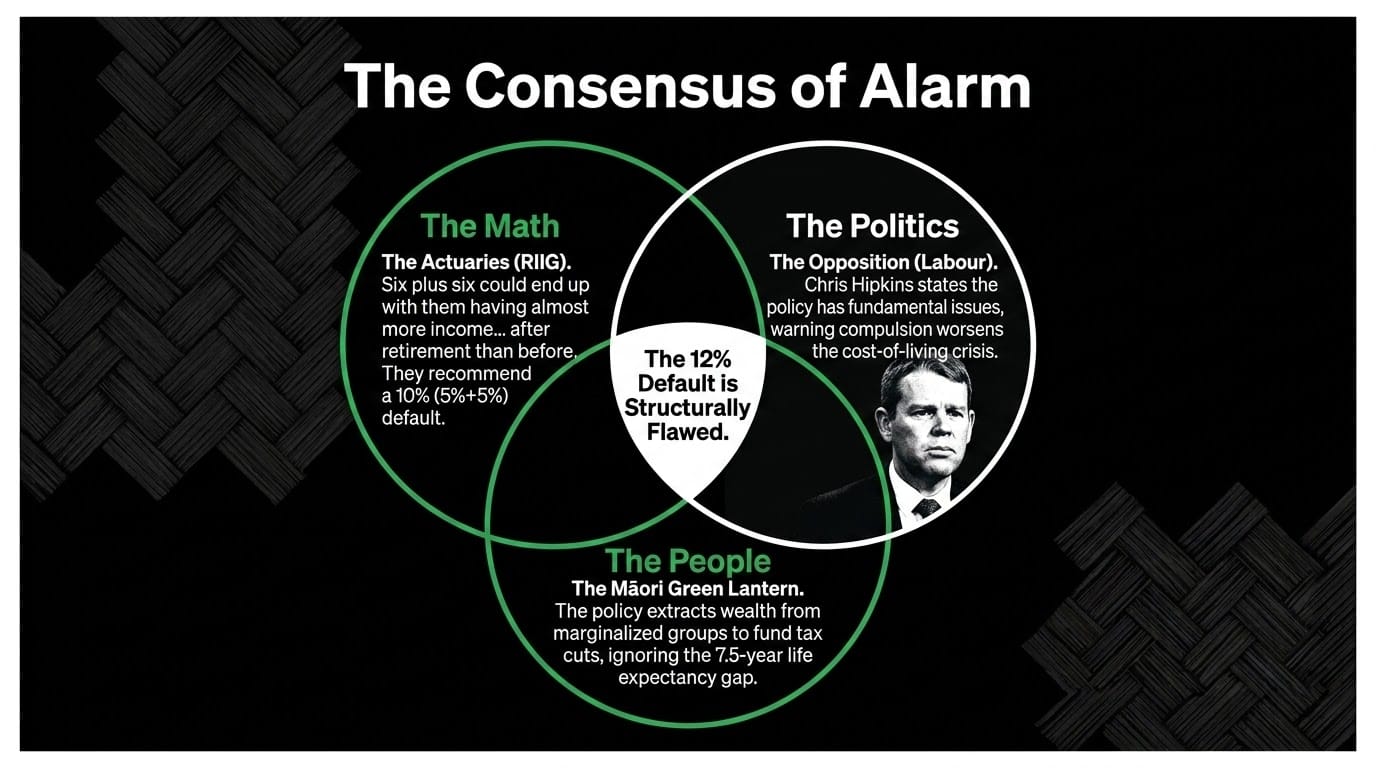

The RIIG report published in the week of 23 June 2026 now provides independent technical confirmation of this exact finding. The actuaries — the professional body whose job it is to model retirement outcomes — found that "the dial is currently set with median and higher earners in mind rather than the people at the bottom." Their finding for minimum wage earners is precise: a combined 12% contribution rate "could result in them having higher spending capacity after retirement than before retirement" — meaning the system extracts more from their working life than it returns in proportional benefit.

This is not an ideological position. It is a technical finding from the NZ Society of Actuaries. And it directly confirms what the Retirement Commission's own data on Māori contribution gaps has been saying for years: the architecture of KiwiSaver penalises those with the lowest wages — which, by structural design of this colonial economy, disproportionately means Māori and Pacific workers.

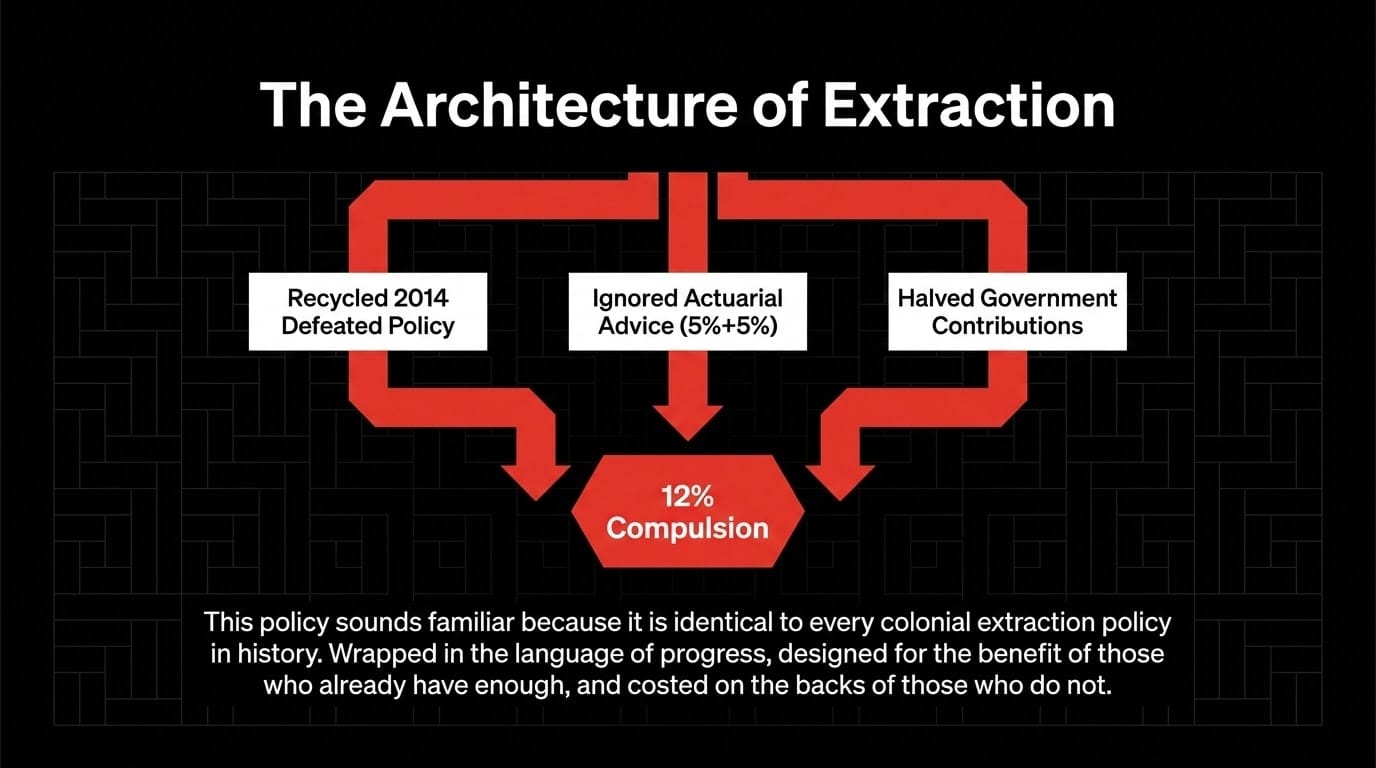

The RIIG finding that Luxon's team should have been asked about, and wasn't: Their 2025 analysis — reconfirmed in June 2026 — recommends a default of 5% member plus 5% employer contribution, not 6%+6%. National is pursuing a rate the actuaries' own modelling does not support.

The Life Expectancy Gap: The Violence the Actuaries Don't Name

Stats NZ data confirms life expectancy at birth for Māori males was 73.4 years (2017–2019), compared to 80.9 years for non-Māori males — a gap of 7.5 years.

The RIIG's model measures adequacy as a replacement rate of 80–100% of after-tax income, with money lasting to at least age 90. That is a benchmark designed for a population whose average life expectancy exceeds 80. It is not designed for a population whose males die, on average, at 73.4. When National raises the super age to 67 — confirmed in National's own published senior commitments — Māori men will have, statistically, just over six years of superannuation.

Every Māori man who dies at 66 receives nothing from a system he contributed to his entire working life. Te Ara Ahunga Ora's 2022 research confirmed: raising the super age would cost Māori men over $200,000 each in missed payments. Neither the actuaries' article nor Labour's response named this number. This essay does.

The Gender Gap

Te Ara Ahunga Ora's research across 3.2 million members found the average gender KiwiSaver retirement savings gap remains at 25%, static since 2022 — with women holding around $20,000 less than men at retirement. AUT Professor Gail Pacheco's research found a 36% gap between the amount men and women contribute each year — driven not by different rates but by the underlying gender pay gap. The Spinoff's 2026 data confirms it persists: men's average KiwiSaver balance is $47,452 versus women's $38,212.

Compulsory KiwiSaver will not close these gaps. It will compel Māori wāhine — who face both the ethnicity pay gap and the gender pay gap simultaneously — to contribute a larger percentage of their already smaller incomes to a system that structurally disadvantages them.

The Low-Income Trap — Now Confirmed by the Actuaries and Labour

The Retirement Commission's own distributional analysis is explicit: low-income members will be disproportionately harmed by the Budget 2025 government contribution cuts.

The RIIG goes further — published days after the original essay. Their finding is that for minimum wage earners, the practical concern is acute: "Lower paid workers are the people most likely to reduce or pause their contributions for long stretches, particularly when childcare costs or a mortgage are squeezing the household budget. Every time they do, they walk away from the matching money their employer would otherwise tip in. A higher headline rate raises the stakes of that trade off without changing the underlying problem."

Labour has confirmed the same finding in political terms, naming the impact on low-income workers as one of the "fundamental issues" blocking cross-party consensus.

Three independent sources — this essay, the actuaries, and Labour — now confirm the same structural harm. National's claim that the policy works "irrespective of background" is not just false. It is the opposite of the truth.

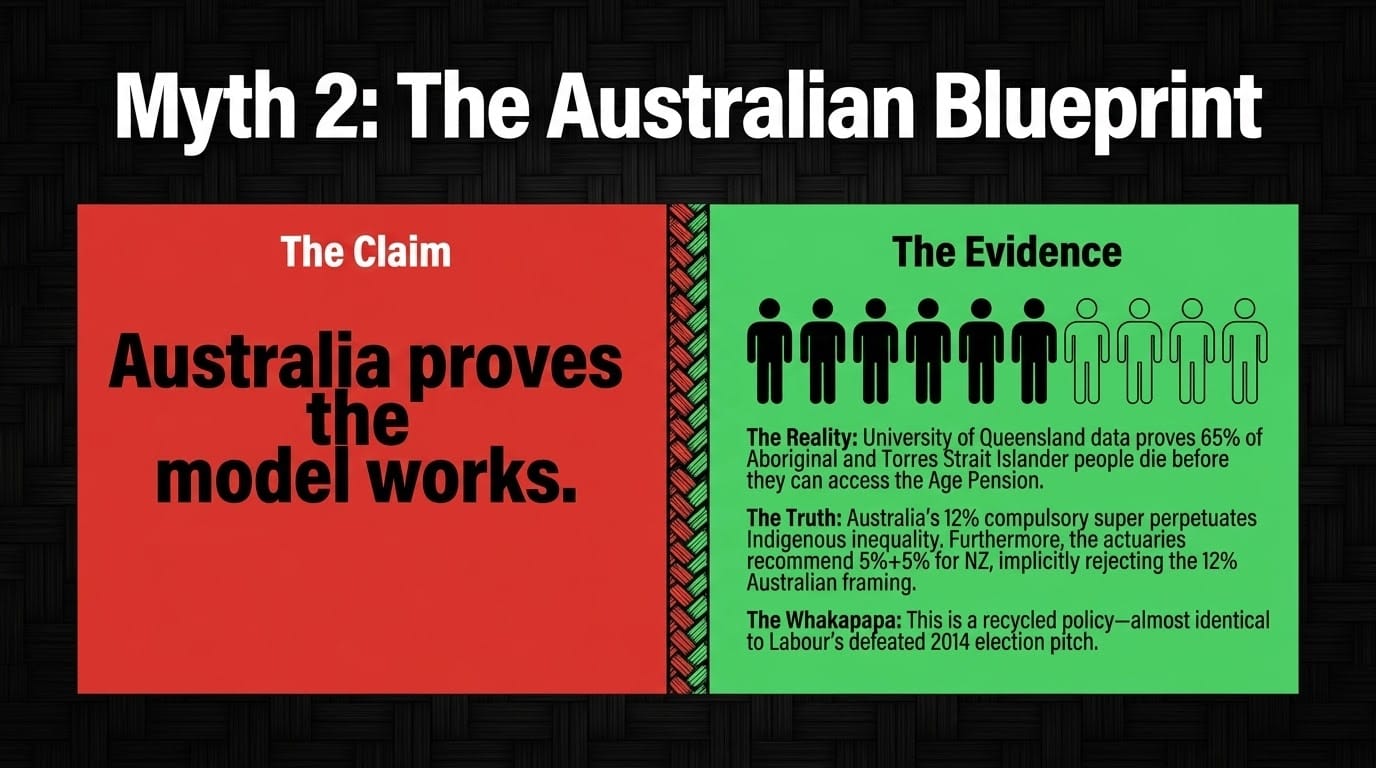

Claim: "Australia Proves the Model Works"

Luxon specifically cited Australia as proof that compulsory superannuation works. Jo Moir's analysis piece accepted this without scrutiny.

University of Queensland research published in 2025 found that 65% of Aboriginal and Torres Strait Islander people die before they can access the Age Pension. Australia's compulsory superannuation system — the very model Luxon is pointing to — was "initially designed for white, male, full-time workers" and "fails to consider factors such as a shorter life expectancy for Indigenous people." ASFA and First Nations Foundation research confirmed: Indigenous people have 23% less in retirement savings on average, and First Nations people earn up to 30% less than non-Indigenous people.

New Zealand's own Retirement Commission research comparing the two systems found explicitly: "Australia's greater reliance on private savings perpetuates inequalities from working years."

The Actuaries Reject the "Match Australia" Target

The RIIG's June 2026 report lands here with precise technical force. Their modelling found that 12% — the Australian rate that National explicitly pledges to match — "might be over-egging retirement savings for middle NZ." Their own recommended default remains 5%+5%, not 6%+6%.

The actuaries are not arguing against higher saving. Their point is surgical: the right answer is unlikely to be the same number for a checkout worker and a chief executive. A single national dial, turned to 12%, produces radically different outcomes across income levels. And it was set, as their report confirms, with the median and higher earners in mind — not the people at the bottom.

Luxon is citing a country whose compulsory savings model has failed its Indigenous people as the blueprint for Māori — and the technical body whose job it is to assess that model has now said the rate he's proposing is too high for most New Zealanders.

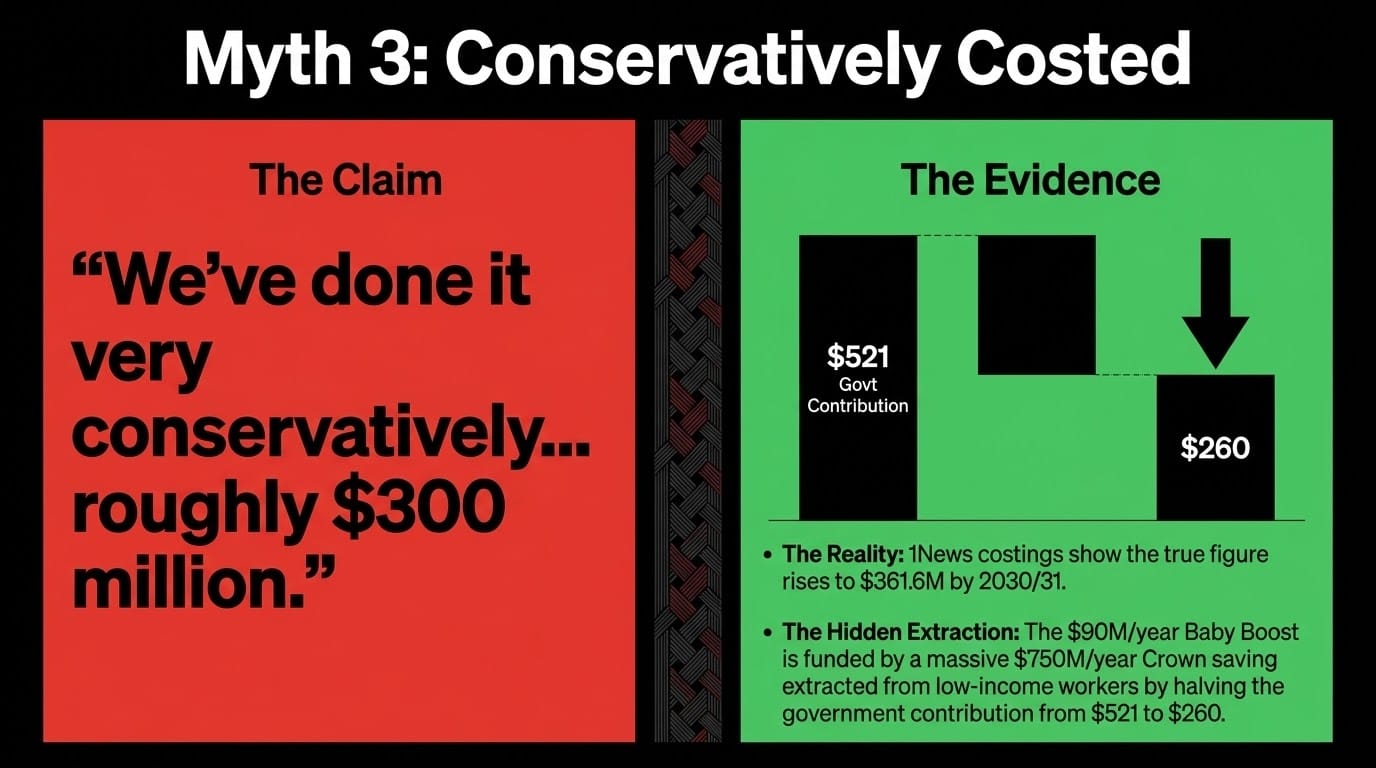

Claim: "We've Done It Very Conservatively in Terms of How We've Costed It"

Luxon told Morning Report the cost was "roughly about $300 million a year" and that it had been done "very conservatively."

1News reported the actual costing: $110.1 million in 2027/28, rising to $323.4 million in 2028/29, $342.2 million in 2029/30, and $361.6 million by 2030/31. This is not "around $300 million." It is a rising commitment breaching $361 million within the forecast period — from a government that in the same Budget:

- Halved the government KiwiSaver contribution, saving hundreds of millions per year

- Abolished Te Aka Whai Ora — the Māori Health Authority — which cost $98 million per year to operate

- Oversaw 169,300 tamariki at a 10-year hardship high

- Committed to a $2.6 billion military helicopter purchase with nothing new for Māori housing

The Baby Boost payment is $90 million per year. The Māori Health Authority that this government abolished cost $98 million per year. They found the money to destroy the one institution built to close the health gap. They found the money for photo-ready baby savings accounts. The receipt is in your pocket, whānau.

Claim: "Difficult for Other Parties to Argue Against This"

Luxon told Morning Report it would be "difficult for other parties to argue against" his KiwiSaver proposals. Jo Moir suggested you'd be hard-pressed "to find a political party in Parliament who doesn't agree with some, if not all, of those pitches."

This is political theatre designed to foreclose debate and shame opposition into silence. It collapsed within 24 hours.

Labour Names the Fundamental Issues

Labour's formal response — as reported by RNZ on 23 June 2026 — declined cross-party consensus and named the specific reasons:

1. The superannuation age linkage. Labour will not support compulsion that is connected — explicitly or implicitly — to a super age rise. As this essay documented using National's own published policies, the super age rise to 67 is already confirmed for 2044. The KiwiSaver announcement is the sweetener for that bitter medicine. Labour has now named the same connection. What Labour has not named — but this essay has — is what that super age rise costs Māori men: over $200,000 each in lifetime entitlements, as confirmed by Te Ara Ahunga Ora's 2022 research.

2. The government contribution cut. Labour correctly identifies the contradiction: you cannot simultaneously cut the government contribution and demand higher compulsory worker contributions. Chris Hipkins confirmed an 18-year-old entering the workforce under these changes will be $66,000 worse off at retirement than before Budget 2025. The Retirement Commission's own distributional analysis confirms this hits low-income earners hardest — for whom the government contribution represented 15–20% of their projected KiwiSaver balance.

3. Equity for low-income workers. Labour names compulsion as too blunt for financially stretched workers — the same finding the actuaries reached through technical modelling.

What Labour's Critique Misses

Labour's position is right as far as it goes. But it is still fundamentally Pākehā-centred in its framing — treating income as the primary axis of disadvantage. It does not address:

- The 7.5-year Māori male life expectancy gap and what that means for compulsory lifetime contributions into a system calibrated for a longer life

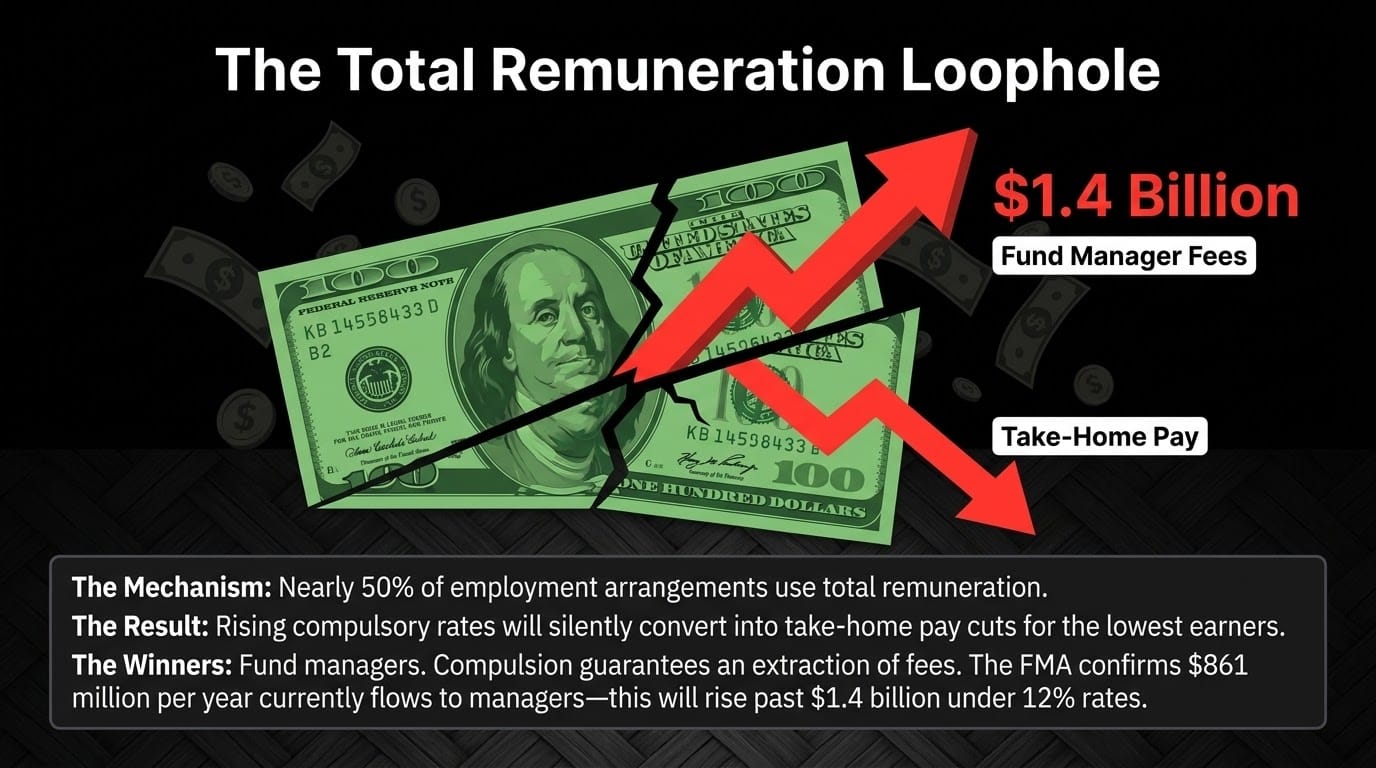

- The near-half of employers using total remuneration arrangements that will silently convert rising compulsory rates into take-home pay cuts

- The $861 million per year flowing to fund managers in fees — growing to an estimated $1.4 billion under compulsory 12% — and the absence of any fee cap in Labour's stated position

- The Australian evidence that compulsory super has perpetuated Indigenous retirement savings inequality, which Labour has not cited

Labour is doing parliamentary accountability work. This essay is doing tikanga accountability work. These are not the same thing, and the difference matters.

ACT and NZ First

ACT's David Seymour had "questions over National's previous plan to lift default contributions" and ACT has historically opposed any KiwiSaver changes requiring increased employer or government contributions. The Spinoff confirmed ACT "has long been opposed to any KiwiSaver changes that would increase employer or government contributions." NZ First's position — a 10% target, not 12%, with automatic enrolment at birth — diverges from National's in rate and structure.

Jo Moir's own analysis noted it clearly, then promptly buried it: "Personal responsibility is one of the key pillars of the National Party's existence, which makes forcing people to join KiwiSaver a tad off-brand." This is not a footnote. This is the whole story. National has spent three decades insisting individuals bear the cost of their own poverty — now demanding the state compel workers to save for a retirement they may not live to receive, while halving the very government contribution that made the scheme worthwhile for people on low incomes.

The Policy Is Recycled — And Was Previously Defeated

The Spinoff's Bulletin on 22 June 2026 delivered a finding that the two original RNZ articles entirely missed: National's compulsory KiwiSaver proposal is "almost identical to Labour's ill-fated 2014 election policy," which promised:

- Compulsory KiwiSaver for every employee aged 18 to 65 from 2014

- Gradual increase of employer contributions at 0.5% per year from 3% to 7% over nine years

The Spinoff's reporting is precise: "The policy was criticised by National at the time. Labour suffered an historic defeat, and three years later, both parties united in campaign promises to not make the scheme compulsory."

National attacked Labour for this policy in 2014. They campaigned against it. Both parties then agreed not to implement it. National now owns it — and presents it as bold vision. This is not policy innovation. This is electoral recycling of a defeated platform, packaged in a conference hall and presented to journalists who did not check the archive.

The Hidden Architecture: Salary Sacrifice and the Wage Theft Nobody's Talking About

Neither RNZ article raises the most dangerous structural risk embedded in compulsory KiwiSaver. Neither does Labour's critique. Neither does the RIIG's technical modelling. But it will fall hardest on low-income, casual, and Māori workers.

Under NZ employment law, employers may use "total remuneration" arrangements where the employer's KiwiSaver contribution comes out of the employee's pay rather than on top of it. Employment Hero confirms: "Salary sacrifice is a mutual arrangement, where an employee agrees to forgo part of their pre-tax salary in return for benefits."

The Retirement Commission's own policy brief on KiwiSaver Total Remuneration is blunt: "The annual amount contributed to KiwiSaver will be lower under a total remuneration model due to the reduced earnings figure." As contribution rates rise compulsorily to 12% by 2032, employers using these arrangements can use rising KiwiSaver obligations to suppress base wages — transferring cost from employer to worker while appearing to comply.

The RIIG's own finding reinforces the trap: low wage earners are the most likely to pause contributions when household budgets are squeezed — "every time they do, they walk away from the matching money their employer would otherwise tip in." Under total remuneration, that employer match is already being drawn from their gross wages. They are contributing their own money twice.

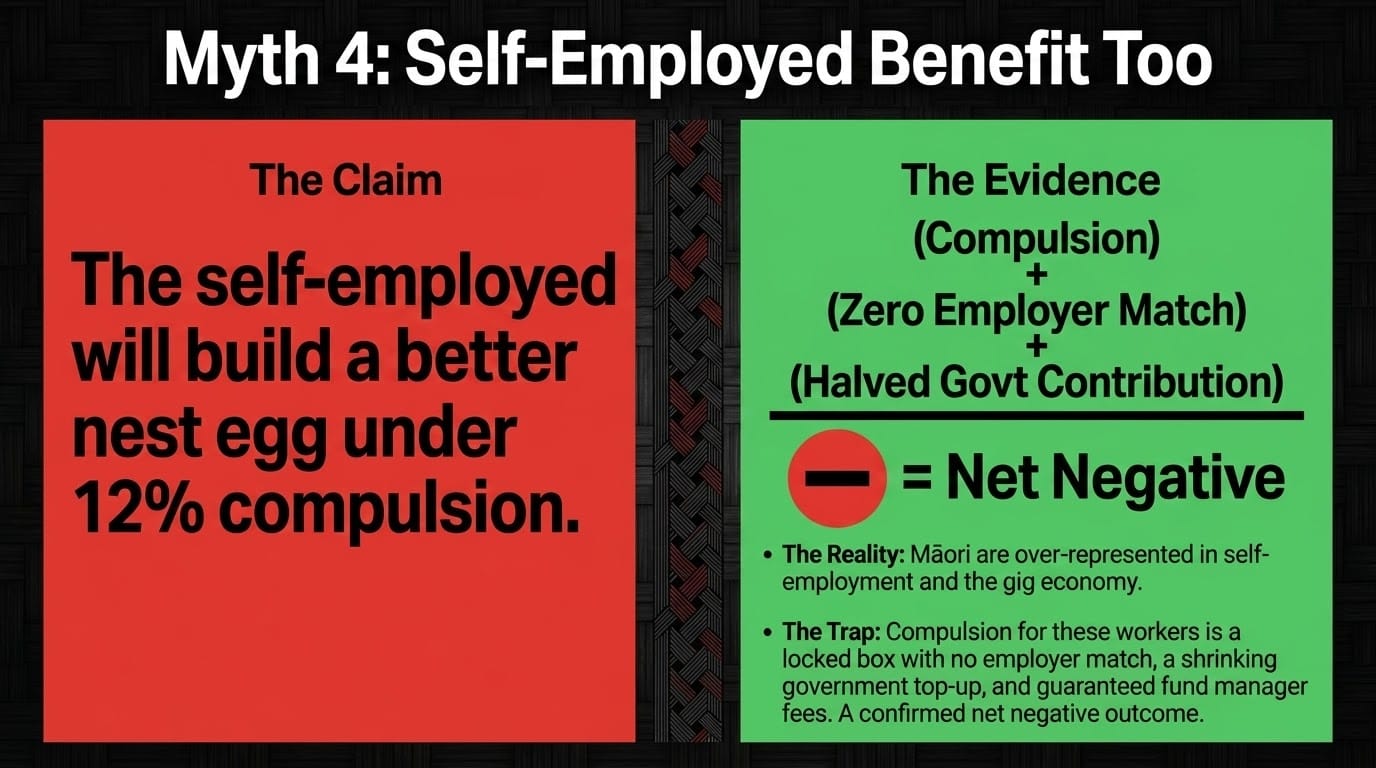

Māori workers are over-represented in low-wage, casualised employment — the exact workplaces where bargaining power is weakest and total remuneration arrangements most prevalent. National has announced no prohibition on salary sacrifice under compulsory KiwiSaver. The Spinoff confirms the self-employed will again be the worst positioned: "Much like now, self-employed New Zealanders will reap the fewest benefits."

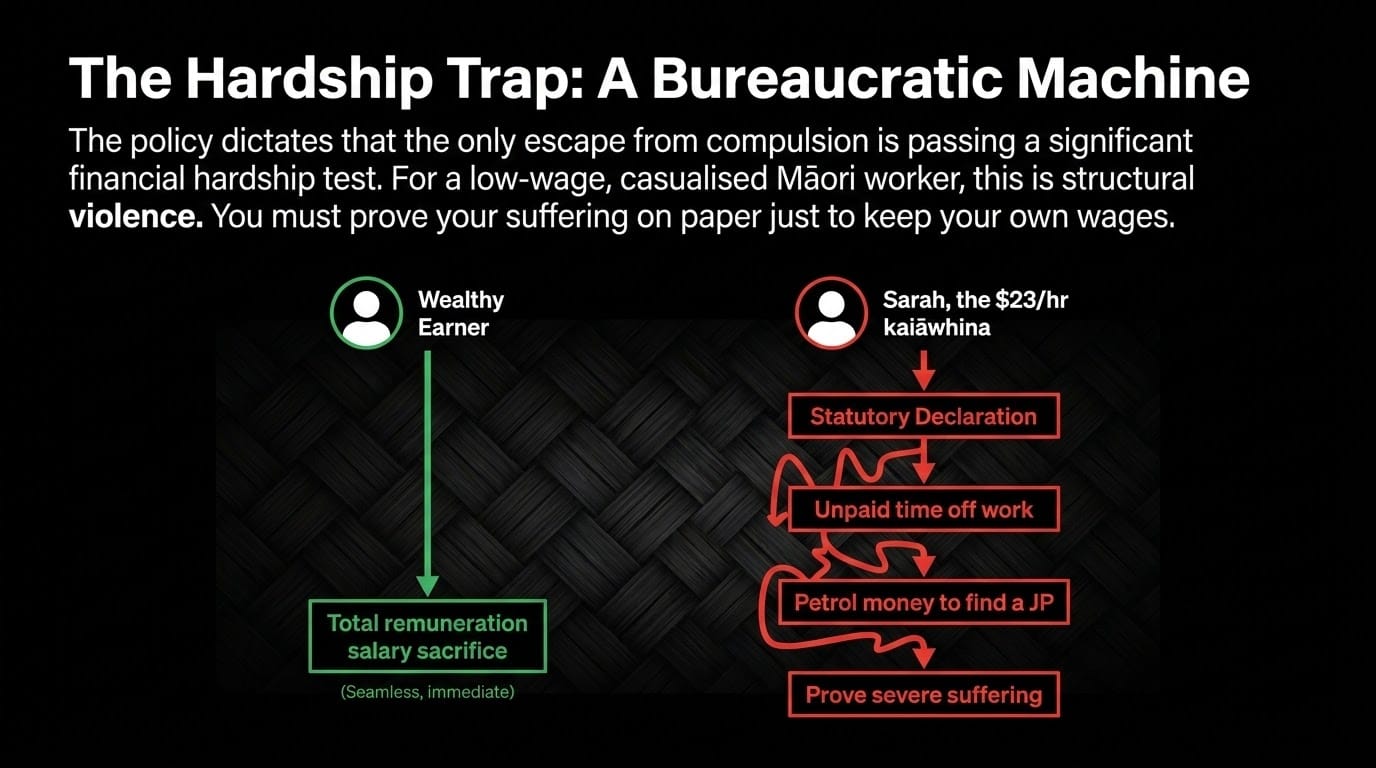

The Hardship Suspension Trap: Bureaucratic Violence in Policy Form

National's own 20 June 2026 policy release confirms: "People will be able to suspend contributions only if they meet the existing hardship test currently used when people apply to make an early withdrawal from their KiwiSaver."

Let me translate that for whānau. The significant financial hardship test is not a "I am struggling" test. It is a statutory declaration — requiring evidence of inability to meet minimum living expenses, mortgage enforcement proceedings, or medical costs requiring immediate treatment. It requires a JP's signature. It requires documentary proof assembled under financial stress.

Sarah in Flaxmere, earning $23 an hour as a kaiāwhina, cannot afford the petrol to get to the JP. She cannot afford to take time off work to gather the evidence. Under compulsory KiwiSaver, she will contribute. The fund manager will charge 0.7%. The government will keep the $260.72 that used to be $521.43. Her employer may use the rising rate to suppress her base wage. And she will have no practical exit.

The RIIG confirms this is not hypothetical: lower paid workers are the most likely to need relief from contribution pressure, and they are also the ones for whom the consequences of pausing are most severe. But National has designed a system where the only relief valve requires proving your suffering meets a statutory threshold.

Neither the actuaries' article nor Labour's response named this specific trap. This essay names it.

The Superannuation Age Trap: The Real Agenda Behind the Announcement

Both original RNZ articles acknowledged this — one carefully, one with conspicuous enthusiasm.

Jo Moir was explicit: the KiwiSaver announcement "laid the groundwork" for National to raise the superannuation age. Finance Minister Nicola Willis "used an unusual amount of her time on Budget Day talking about superannuation" and has suggested parties who don't act on the entitlement age "are robbing future generations." National's published senior commitments confirm: the super age will rise to 67 from 2044, affecting everyone born from 1979.

This is the sequence:

- Make KiwiSaver compulsory — generating popular support and political cover

- Point to expanded KiwiSaver as justification for raising the super age

- Raise the super age from 65 to 67 — saving approximately $2.7 billion annually at today's prices

Labour has now formally named the super age linkage as a "fundamental issue." Labour is correct. But Labour has not quantified what that linkage costs Māori men — because that number is politically uncomfortable for every party.

This essay has: Over $200,000 each in missed entitlements. Tens of thousands of Māori men who will never reach 67. A compulsory savings scheme that asks them to contribute faithfully to a retirement the system is structurally designed to deny them.

Five Hidden Connections: The Whakapapa of This Policy

These five connections were established in the original essay. They are reinforced, not undermined, by 24 hours of new evidence.

- The same hand that cut, now promises to restore. National cut the government KiwiSaver contribution four times since 2011. The RIIG's finding — that the current default is already set for median earners, not the bottom — confirms the system National built and then repeatedly cut was never designed for whānau. The net beneficiaries of compulsion at 12% are fund managers, not workers. Verified.

- KiwiSaver was never designed for Māori. MSD's own 2009 research found KiwiSaver's tax incentives "will tend to raise inequality" and benefit higher-income earners disproportionately. The RIIG's 2026 report confirms the architecture has not changed. Verified.

- Australia's model Luxon cites is failing its Indigenous people. UQ research, confirmed by ASFA, confirmed by the Super Members Council — and now implicitly rejected by the RIIG, who recommend a lower rate than Australia's. Verified.

- The policy is designed to sell a super age rise that will cost Māori over $200,000 each. Labour has now named the super age linkage. National has published the policy. The Te Ara Ahunga Ora harm estimate is on the record. Verified.

- Compulsory KiwiSaver without wage protections enables salary sacrifice wage suppression. The RIIG confirms low earners are most likely to pause contributions under financial pressure — and under total remuneration, those pauses cost them twice. Corroborated.

The Quantified Harm to Whānau

| Harm | Data | Source |

|---|---|---|

| Government KiwiSaver contribution cut 2025 | From $521.43 to $260.72 annually | IRD / Budget 2025 |

| Māori/Pacific annual contribution gap vs European | ~$1,500 less per year | Te Ara Ahunga Ora |

| Gender KiwiSaver balance gap | 25% / ~$20,000 less for women near retirement | Te Ara Ahunga Ora |

| Māori male life expectancy vs non-Māori male | 73.4 years vs 80.9 years (7.5-year gap) | Stats NZ 2017–2019 |

| Māori men's lost super if age raised to 67 | Over $200,000 in missed payments | Te Ara Ahunga Ora |

| 18-year-old loss at retirement under Budget 2025 changes | $66,000 worse off | Labour / Retirement Commission |

| National's KiwiSaver cuts 2011–2025 | $500M+ p.a. stripped from MTC; $500M from Kick-Start; govt contribution halved twice | Beehive / Green Party |

| RIIG recommended rate vs National's target | 5%+5% recommended; 6%+6% proposed | NZSA RIIG |

| 12% rate impact on minimum wage earners | Could leave them with higher spending capacity in retirement than during working life | RIIG / Newswire |

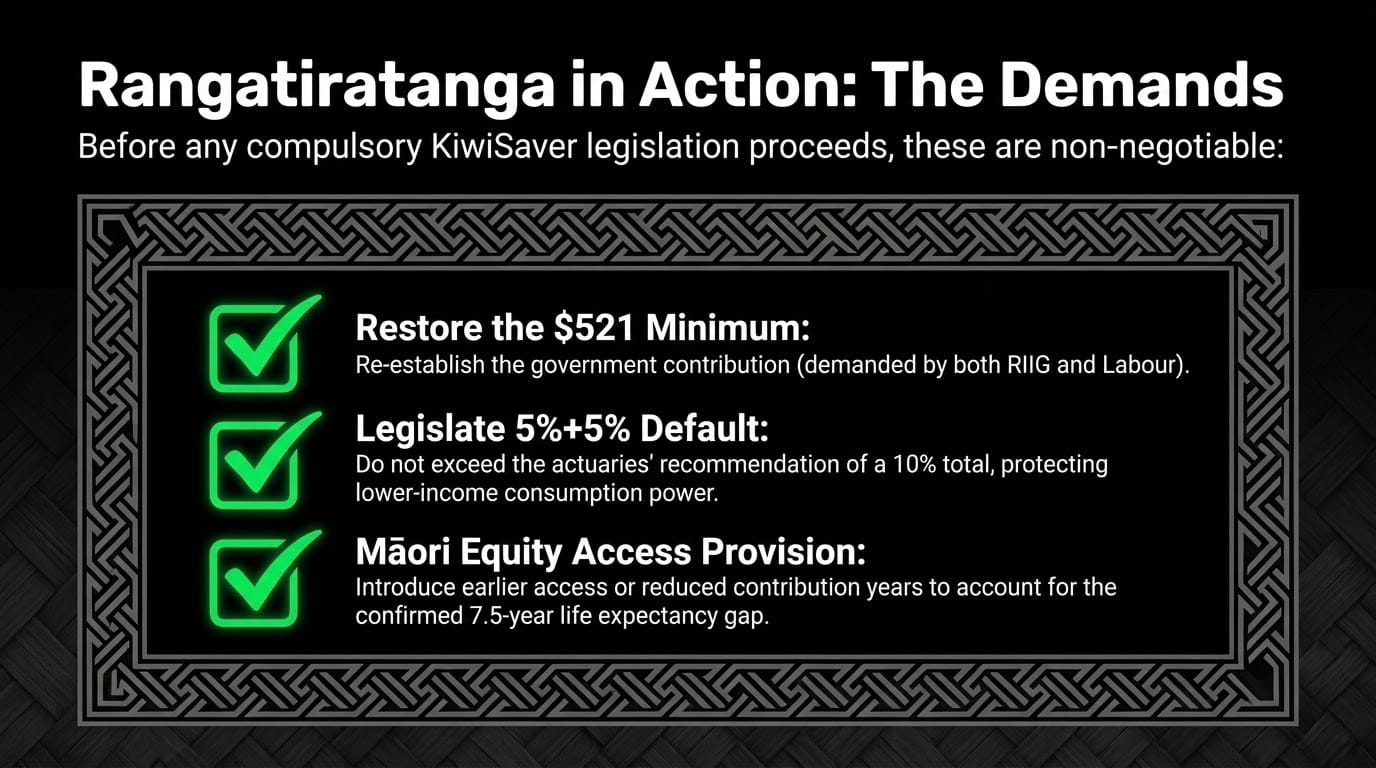

What Rangatiratanga Actually Demands

Compulsory KiwiSaver is not wrong in principle. The principle — that workers should build retirement savings over their lifetime — is sound. But a policy that ignores Māori life expectancy, raises contributions while cutting government top-ups, uses compulsion to mask a super age rise, does nothing about structural pay gaps, and asks minimum wage workers to save at a rate the actuaries themselves call excessive — that policy is not "common sense." It is structural racism wearing a clipboard.

What rangatiratanga actually demands — and what neither the actuaries' article nor Labour's response has required:

- Restore the government contribution to at least $521 — reversing the Budget 2025 cut. Source: IRD, Retirement Commission distributional analysis

- Legislate 5%+5% as the default, not 6%+6% — consistent with the RIIG's own recommendation. Source: RIIG/NZSA

- Introduce a Māori equity access provision — earlier access or reduced contribution years reflecting the 7.5-year life expectancy gap. Source: Stats NZ, Hāpai Te Hauora

- Prohibit total remuneration salary sacrifice for compulsory contributions. Source: Retirement Commission Total Remuneration Policy Brief

- Replace the hardship suspension test with an accessible low-income opt-down mechanism — consistent with the RIIG finding that 6% is excessive for minimum wage earners. Source: RIIG/Newswire

- Cap fund management fees at a regulated maximum. Source: FMA Annual Report 2025

- Publish a full Te Tiriti impact assessment of the proposed super age rise before any compulsion legislation is tabled. Source: Te Ara Ahunga Ora 2022 research

He Mana Tō Te Tūtū

Jo Moir wrote that "this is a policy whose time has come." But policies do not come in their own time — they are shaped by power, sold through narrative, and measured by whose mauri they lift and whose they drain.

In 24 hours, the professional actuaries and the parliamentary opposition both confirmed the core of what this essay argued with primary evidence.

Neither group named it in the language of tikanga. Neither group used the word "extraction." Neither group traced the whakapapa of four consecutive cuts followed by a compulsory demand. Neither group named the man on $21–30 million in property assets asking the kaiāwhina in Flaxmere to lock more of her $23/hour wage into a fund manager's account.

But both groups said, in their own register: this policy, as designed, will harm the lowest earners most.

And I say: the lowest earners in New Zealand are, disproportionately, Māori. They are wāhine. They are Pacific. They are tamariki of the 25.1% in material hardship. They are Te Koha on his bad knees in Rotorua, 58 years old, contributing faithfully to a scheme whose government top-up was just halved, whose contribution rate is rising, whose super age is planned to move beyond his actuarial life expectancy.

The Spinoff confirmed that National's proposal "sounds familiar" — because it is almost identical to the policy both parties walked away from in 2014. It sounds familiar to me for a different reason: it sounds exactly like every colonial extraction policy in New Zealand history — wrapped in the language of progress, designed for the benefit of those who already have enough, and costed on the backs of those who do not.

The trough is still full. It is not being filled for you.

Kāo ki tēnā. No to that.

Ko tō tātou hīkoi ki te ao mārama — our journey to the world of light — requires we name every chain.

Whakaaro whānui — think wide, whānau. The conjurer's trick only works if nobody watches his other hand.

Kia kaha, whānau. Stay vigilant. Stay connected.

Koha — Every Act of Support Is Rangatiratanga

While the actuaries model the damage in technical terms, and Labour names it in parliamentary terms, this essay named it first — in tikanga terms — because whānau-funded, independent accountability work goes where professional liability and parliamentary privilege cannot.

Every contribution to The Māori Green Lantern is a signal that we are ready to support our own truth tellers. That we understand that the $861 million per year flowing to fund managers, the $260 where $521 used to be, the 25.1% of tamariki Māori in material hardship — none of this will be changed by people who depend on those same structures for their income.

Kia kaha, whānau. Stay vigilant. Stay connected. If you are able, consider a koha to keep this taiaha sharp.

If you cannot koha — no worries at all. Subscribe, follow, share with your whānau. That circulation is the hau returning.

💚 Koha directly: https://app.koha.kiwi/events/the-maori-green-lantern-fighting-misinformation-and-disinformation-ivor-jones

📬 Subscribe to receive essays directly: https://www.themaorigreenlantern.maori.nz/#/portal/support

🏦 Direct bank transfer: HTDM — Account 03-1546-0415173-000

📘 Facebook: https://www.facebook.com/Themaorigreenlantern/subscribe/

Disclaimer: This essay is published in the public interest pursuant to qualified privilege under the New Zealand Defamation Act 1992, consistent with the principles established in Lange v Atkinson 3 NZLR 385. All factual claims are supported by cited primary sources, government publications, or peer-reviewed research. Named individuals are referenced exclusively in their public capacity as elected officials or public figures. All opinions are clearly flagged as such and grounded in the stated evidence base. Any factual error will be corrected upon notification. No malice is asserted or intended.